The Bank of Ireland Platinum Credit Card is a premium Ireland credit card designed for people who want extra travel and purchase protections alongside everyday spending flexibility. This short introduction explains the purpose of the article and outlines what you will learn about how to apply, eligibility, fees and benefits. It is written for salaried employees, the self-employed and frequent travellers in the Republic of Ireland.

Platinum Credit Card

The guide will show step‑by‑step how to apply for Platinum card status, what to expect from a Bank of Ireland credit card application and practical timelines from submission to receipt of the card. Where rates or charges are discussed, check Bank of Ireland’s website or the Central Bank of Ireland guidance for the latest figures.

Anúncios

Key Takeaways

- Learn simple steps to complete a Bank of Ireland credit card application online or by other channels.

- Understand the main eligibility requirements for the Bank of Ireland Platinum Credit Card.

- Know which documents you will typically need for income, ID and address verification.

- Get a realistic timeline from application to card delivery so you can plan travel or purchases.

- Compare core benefits and fees before you decide to apply for Platinum card status.

IRELAND: STEP-BY-STEP GUIDE – How to Apply for the Bank of Ireland Platinum Credit Card

If you’re seeking a credit card with a lower interest rate and added insurance features, this guide walks you through the process of applying for the Bank of Ireland Platinum Credit Card.

Why Consider the Platinum Credit Card?

The Bank of Ireland Platinum Credit Card is positioned as the bank’s low-rate premium option.

It offers:

Anúncios

- A lower standard purchase APR compared to the Classic Card

- Worldwide multi-trip travel insurance

- Additional protections and premium benefits

Before You Apply: Eligibility Requirements

To apply, you must:

- Be at least 18 years old

- Reside in the Republic of Ireland

- Meet BOI’s lending criteria, including sufficient proof of income

- Provide documentation for identity, address, and income verification

Important: The Platinum Card carries an Annual Account Fee (around €76.18) in addition to the Government Stamp Duty of €30.

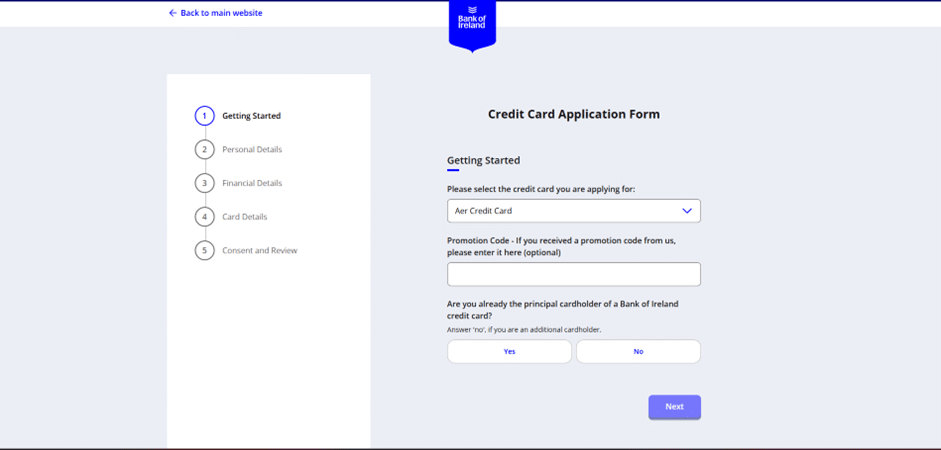

Step 1: Go to the Bank of Ireland Credit Cards Section

Start by visiting the Bank of Ireland website.

- Open the Bank of Ireland Personal Banking homepage.

- In the main navigation bar, select “Borrow” (or “Products”, depending on the layout).

- From the submenu, choose “Credit Cards”, then click “View all” or “Compare Credit Cards”.

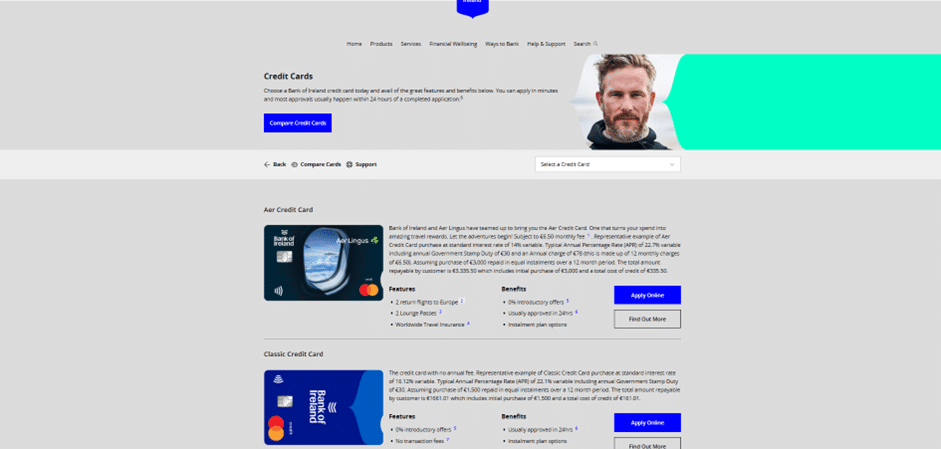

Step 2: Choose the Platinum Credit Card

On the credit card comparison page, look for the Platinum Credit Card.

You’ll see several options—Classic, Aer, and Student.

- Select Platinum (usually the third option)

- Click “Find out more” to access the product details

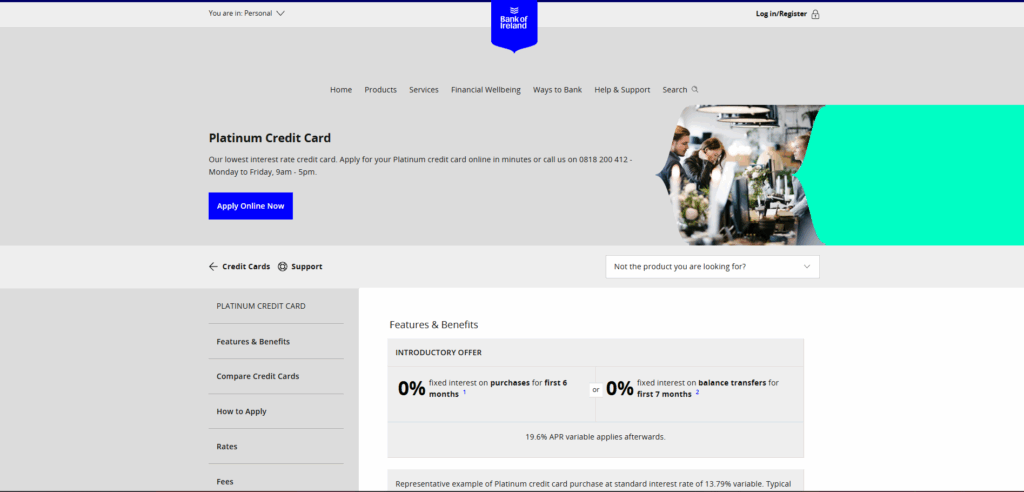

Step 3: Start Your Online Application

You will now be on the Platinum Card’s detailed information page.

Here you will find:

- Representative APR: 19.6% variable

- Introductory promotions (often 0% for 6 months on purchases or 0% for 7 months on balance transfers)

To begin your application, click the blue “Apply Online Now” button.

Step 4: Complete the Application Process

You will be redirected to BOI’s online application system.

- If you are already a Bank of Ireland customer using 365 Online, the process will be faster. Approvals for existing users typically occur within 24 working hours.

- Enter your personal, financial, and income details as requested.

- Upload your required documents following the on-screen instructions.

Once finished, submit the application for review. The bank will contact you with the result of your Platinum Credit Card application.

Overview of the Bank of Ireland Platinum Credit Card

The Bank of Ireland Platinum Credit Card is marketed as a premium credit card Ireland customers turn to for elevated protection and greater spending flexibility. Cardholders can expect higher credit limits than standard cards, contactless and chip-and-PIN security, plus worldwide acceptance on the applicable Mastercard or Visa network listed on the product page.

What the Platinum card offers

Typical Platinum card features include travel insurance, purchase protection and extended warranty cover that apply to eligible purchases. Many versions add concierge or travel assistance services, online account management, paperless statements and the option of supplementary cards for household members, subject to eligibility and any fees.

Who the card is suitable for in Ireland

This product suits people with stable incomes and good credit histories who need enhanced travel protections and higher limits. Frequent travellers benefit from overseas acceptance and insurance cover. Households wanting a primary card with extra cardholders will find the flexibility useful. Prospective applicants should consider who should get Platinum card based on travel habits, spending levels and appetite for an annual fee in return for perks.

Key differences from other Bank of Ireland cards

In a Bank of Ireland card comparison, the Platinum rank sits above standard credit and debit cards in benefits and eligibility thresholds. Expect higher APRs or an annual fee in exchange for expanded insurance packages and concierge-style benefits. Student or low-fee cards typically offer lower limits and simpler reward structures, while the Platinum product emphasises perks, protection and premium service.

Card features and benefits can change over time. Applicants should review Bank of Ireland’s official product page and full terms and conditions to confirm the exact insurance packages, APR and fees that apply when they apply.

Bank of Irland

Bank of Ireland Platinum Credit Card — learn how to apply for this card.

Starting an application is straightforward. Visit Bank of Ireland’s official site, open the Credit Cards section and choose the Platinum Credit Card page. Use the “Apply” or “Check eligibility” options to begin. You will need to complete the form with personal details, income and employment information and give consent for a credit check.

Have digital copies of proof of ID, proof of address and proof of income ready. The site may prompt you to upload these documents during the process. A clear photo or scanned PDF speeds verification and reduces delays in the credit card timeline.

Not everyone prefers online forms. For a branch application, call ahead to book a meeting at your local Bank of Ireland branch. Staff can check your documents in person and explain any points you find confusing. A face-to-face visit works well when you need help gathering paperwork or want reassurance about eligibility.

You can also apply by phone through Bank of Ireland’s customer services. An advisor will guide you through the questions, perform basic eligibility checks and note any documents you must supply. Phone applications suit applicants who prefer to talk through finance decisions rather than complete an online form.

Expect an initial decision quickly when you apply online Bank of Ireland. Many applicants see an instant result. If the bank needs further verification, the decision can take a few working days. Complex income checks or overseas residency questions extend the credit card timeline.

Once approved, card dispatch usually takes several working days up to one to two weeks. The receive card timeframe varies with postage and verification steps. Activate the card on arrival by phone, online banking or at an ATM to start using it.

Practical tips improve your chance of smooth processing. Provide accurate contact details and an active email, check spam folders for bank messages and be ready for a soft or hard credit search. Keep copies of documents to hand so you can respond quickly to any verification requests.

| Application Channel | How to Start | Typical Decision Time | Receive Card Timeframe |

|---|---|---|---|

| Apply online Bank of Ireland | Visit Credit Cards page, select Platinum, complete form and upload documents | Instant to a few working days | Several working days to 1–2 weeks |

| Branch application | Book appointment, bring originals of ID, address and income proof | Same day to a few working days | Several working days to 1–2 weeks |

| Apply by phone | Call customer services, answer advisor questions, send documents if requested | A few working days | Several working days to 1–2 weeks |

Eligibility criteria and required documentation

Before you apply, check the basic eligibility Bank of Ireland Platinum conditions. This short guide covers the age requirement, residency requirement and the usual list of required documents. It also explains what income proof Ireland applicants typically need to show.

Minimum age and residency requirements

The age requirement for most applicants is 18 years or older. Young adults under 18 are not eligible. The residency requirement usually means you must live in the Republic of Ireland and hold a valid PPS number or other national identifier. Recent arrivals or non-residents may face extra checks or could be ineligible depending on Bank of Ireland policy.

Income and employment evidence

Bank of Ireland asks for income proof Ireland to assess affordability and set credit limits. Employed applicants generally provide recent payslips, normally the last two or three months, or a P60/P45 when appropriate. Self-employed customers should submit recent accounts, tax returns or a Revenue Commissioners statement of income.

Household income and employment status are reviewed as part of the affordability test under Central Bank rules. For unusual income sources or high limits, the bank may request further documentation.

Identification and address verification documents

Valid photographic ID is required. Suitable options include a passport, an Irish driving licence or a national identity card. Proof of address must be recent, commonly within three months, and can be a utility bill, bank statement or a local authority letter.

If you apply in branch, originals will be inspected. For online applications, scanned or photographed copies may be uploaded. Supplementary cardholders normally need to provide proof of identity and consent.

Additional checks

A credit history check through Irish bureau systems forms part of the assessment. The bank will verify required documents and may ask for extra papers if any detail is unclear. Keep payslips, tax documents and proof of address ready to speed up a decision.

Understanding fees, rates and interest charges

Knowing how fees and interest work helps you use a Bank of Ireland Platinum card with confidence. Read the published Key Facts Document and Terms and Conditions for exact numbers before you apply.

Representative APR and how it works

The representative APR gives a clear view of the typical annual cost of borrowing. It combines interest with certain fees to show what a borrower might pay over a year when balances are carried past the payment due date.

What you are offered can differ from the published figure. Creditworthiness and the current product rate influence the exact rate. Ask Bank of Ireland for examples of monthly repayments at different balances to see the practical effect of the Platinum APR and to understand the representative APR explanation fully.

Annual fees and additional cardholder charges

Some premium cards carry an annual fee. Check whether the Platinum card has an annual fee credit card charge and whether supplementary cardholders incur extra costs.

Other possible charges include replacement card fees, fees for paper statements and card upgrades. The product page lists up-to-date amounts. Review that section to avoid surprises.

Cash advance fees and foreign transaction charges

Cash advances usually attract a cash advance fee, either a fixed amount or a percentage of the amount withdrawn. Interest on cash advances typically starts on the date of withdrawal and continues until repayment.

Purchases made outside the eurozone or in a currency other than euro may incur a foreign transaction charge Ireland, often shown as a percentage of the transaction. Contactless and point-of-sale payments in euro within SEPA are usually free of FX fees, but confirm specifics with the bank.

Late payment, default charges and interest calculation

Missing payments can lead to late payment fees and higher penalty interest rates. Repeated defaults may affect your credit record with Irish credit reference agencies.

Interest on carried balances is calculated daily on the outstanding balance and applied according to the card’s billing cycle. For transparency, ask for worked examples that show interest and fees for different repayment behaviours.

Regulatory context and where to check details

Central Bank of Ireland rules require clear disclosure of fees and APRs. Always consult the Key Facts Document and request any clarification from Bank of Ireland staff before committing to a card.

| Charge type | Typical structure | What to check |

|---|---|---|

| Platinum APR | Published representative rate; may vary by applicant | Representative APR explanation and examples of monthly repayments |

| Annual fee | Fixed yearly charge for some premium cards | Whether the card is an annual fee credit card and costs for supplementary cards |

| Cash advance fee | Fixed fee or percentage; interest from withdrawal date | Exact fee amount and interest calculation method |

| Foreign transaction charge Ireland | Percentage of non-euro transactions or out-of-SEPA purchases | Rates for non-euro spending and SEPA exceptions |

| Late/default charges | Flat late fee plus possible higher interest | Amounts, penalty APRs and impact on credit record |

Benefits and rewards of the Platinum Credit Card

Platinum card benefits often appeal to travellers and frequent shoppers. Cardholders expect a mix of protections, perks and services that add value beyond standard cards. Read the product terms before relying on any specific benefit.

Travel and purchase protection features

Many premium cards include travel insurance when you pay for a trip with the card. Cover typically depends on residency, age limits and how the booking is made. Policies commonly include lost luggage cover, travel delay insurance and emergency medical assistance.

Purchase protection can cover theft or accidental damage for a limited period after purchase. Extended warranty benefits may lengthen a manufacturer’s guarantee on appliances or electronics. Policy details, claim limits and exclusions are set by insurers and can change, so check the issued policy documents before travel or big purchases.

Rewards, offers and partner discounts

Rewards and offers vary by scheme and may include points, cashback or partner discounts at retailers, airlines and restaurants. Some deals come through Visa or Mastercard networks; others arrive via Bank of Ireland promotions. Register for specific promotions and read redemption terms to avoid surprises.

If you travel often, look for partnerships with hotel chains or airlines that boost value. For everyday spending, compare the earn rate against any annual fee to see if rewards justify the cost.

Additional cardholder privileges and concierge services

Extra perks can include priority customer service, a cardholder concierge and, for some cards, airport lounge access. The cardholder concierge may help with restaurant bookings, travel arrangements and event tickets. Not every Platinum-branded card includes these features, so confirm eligibility on Bank of Ireland’s product page.

Airport lounge access and concierge options often depend on the card network and the scheme level. If these services matter to you, verify which lounges and what concierge support are included.

How to claim benefits and assess value

To make a claim keep receipts, boarding passes and any relevant documents. Contact the insurer or Bank of Ireland’s claims team promptly and follow the insurer’s process. Register travel and read benefit guides before booking to ensure cover applies.

Weigh insurance and perks against fees and APR. When benefits match your needs, the card can represent strong value. If you rarely use the protections or concierge, a no-fee or low-fee card might be a better match.

Managing your account: online and mobile banking

Accessing your Bank of Ireland online banking and the mobile app makes day-to-day credit card management much easier. Start with a short setup, link your Platinum Credit Card and choose notification preferences that suit your routine.

Setting up your online access

Begin at the Bank of Ireland website and select Personal Banking registration. Create a strong login, confirm identity with account details and set up security questions. Enable Two-Factor Authentication where offered for added protection.

Once registered, link the Platinum Credit Card to view statements, recent transactions and to make payments. Paperless statements and up-to-date contact details help the bank reach you quickly about any card activity.

Using the mobile app to track spending and pay bills

The mobile app shows real-time transactions and a category breakdown of spending. Use it to download statements, set up Direct Debits and schedule one-off card payments.

Manage supplementary cards, activate a new card, change your PIN or freeze a card temporarily from within the app. These tools help you manage credit card use while on the go.

Security features: alerts, locks and fraud protection

Set payment alerts and transaction notifications by SMS, email or push to watch for unusual activity. Low-balance and large-transaction alerts give early warning if something changes.

The app lets you lock a card instantly if it is lost. Bank of Ireland operates 24/7 fraud monitoring and provides liability protections for unauthorised transactions subject to fair usage and customer responsibilities. Report lost or stolen cards without delay.

Use strong, unique passwords, keep Two-Factor Authentication active and review statements regularly for unfamiliar charges. These habits improve card security Ireland and reduce the chance of fraud while helping you manage credit card finances with confidence.

Tips for a successful application and approval

Applying for the Bank of Ireland Platinum Credit Card goes more smoothly when you prepare. Below are focused steps to help you improve your chances and avoid common pitfalls.

How to improve your creditworthiness before applying

Keep employment steady and show regular income on payslips or pension statements. Lenders value continuity when assessing risk.

Lower your credit utilisation by paying down balances on existing cards. A lower ratio signals better financial management.

Make every payment on time for current accounts, loans and standing orders. Prompt payments build a stronger file with Irish credit reference bodies.

Register on the electoral roll if you qualify. It helps confirm address history and reduces identity mismatches.

Consider a starter product such as a credit-builder card or a small overdraft to establish positive repayment history before applying for a higher-tier card.

Common application mistakes to avoid

Do not enter incorrect personal or financial details. Simple typos in your name, date of birth or income can trigger delays or refusals.

Always declare regular sources of income, including bonuses and rental payments. Omitting income can lead to an incomplete affordability assessment.

Avoid applying for several credit products in quick succession. Multiple hard searches lower your score and raise concerns for underwriters.

Disclose existing debts and active direct debits. Hiding liabilities may cause the application to be declined when checks reveal them.

Submit requested documents promptly. Late responses extend processing times and may count against you if the lender needs up-to-date information.

What to do if your application is declined

Read the reason given by Bank of Ireland carefully. They normally provide a primary cause, such as affordability, credit history or identity issues.

Order a copy of your credit report from the Central Credit Register and, where relevant, from private credit bureaux. Check for errors and mismatches.

Fix any address or identity mismatches by supplying proof, for example a utility bill or PPS number confirmation. Correcting small errors can change the outcome.

Reduce outstanding debt and wait before reapplying. A pause of several months allows repayments to reflect on your record and reduces the impact of recent searches.

Contact Bank of Ireland to request reconsideration or ask about alternative products with lower credit criteria. Keep written records of all correspondence and request a formal reason for refusal under data protection and consumer credit rules.

| Step | Action | Benefit |

|---|---|---|

| 1 | Check payslips and proof of income | Shows stable earnings and improves affordability assessment |

| 2 | Reduce current card balances | Lower credit utilisation boosts score and approval odds |

| 3 | Register on the electoral roll | Improves address verification for the lender |

| 4 | Avoid multiple applications in short time | Prevents multiple hard searches that harm credit standing |

| 5 | Request and review credit reports | Identifies errors and guides declined application steps |

| 6 | Contact the bank for reconsideration or alternatives | May lead to approval on a different product or helpful guidance |

Comparing the Platinum Credit Card with other Irish credit cards

The Bank of Ireland Platinum sits in the premium tier. It adds travel insurance, purchase protection and concierge-style perks that many standard cards do not offer. Premium features often come with a Representative APR and an annual fee that are higher than those on no-fee or low-cost alternatives.

How it stacks up on interest rates and fees

Compare interest and fees by checking the Representative APR and annual charge against products from AIB, Permanent TSB and other Irish issuers. Premium cards usually show higher APRs and an annual fee but bundle cover such as travel insurance and extended warranties. Low fee credit card options or student and basic cards tend to charge little or nothing each year, but they provide fewer added benefits.

Comparative benefits for frequent travellers vs everyday users

Frequent travellers may value the Platinum card for its global acceptance and travel protections. For people who travel often, those perks can offset the cost of an annual fee and make this card the best credit card for travel in some cases.

Everyday users who clear their balance monthly might prefer a low fee credit card or a cashback card. If routine spending is the priority, a card with lower ongoing costs or rewards on groceries and fuel could outperform a premium travel-focused product.

When to choose a different credit card product

Choose an alternative if your main aims are low interest rates, no annual fee or balance transfer offers. A basic credit card or a debit card may suit applicants with limited credit history or low monthly spend. If cash interest and fees top your list, include a low fee credit card in any credit card comparison Ireland exercise.

To make a practical decision, list priorities such as interest, fees, travel cover and rewards. Read Key Facts Documents and terms carefully. Use tools to compare Irish credit cards and speak with a bank adviser when in doubt.

Conclusion

The Bank of Ireland Platinum Credit Card is a premium option that suits people who want higher credit limits, travel and purchase protections, and extra services such as concierge support. To apply for Bank of Ireland Platinum, make sure you meet the eligibility criteria and can provide accurate identification, proof of income and address documents before you start.

Understanding fees, representative APR and cash advance charges is vital. Final thoughts Platinum card: weigh the benefits against any annual fee and verify cover limits in the Key Facts Document and insurance policy terms. Use online and mobile banking tools to manage the account securely and to keep spending under control.

If you decide to apply for Bank of Ireland Platinum, begin the online application on Bank of Ireland’s website or visit a local branch for personalised help. If you are unsure which product to choose, compare options to choose credit card Ireland that best fits your travel habits and everyday needs before committing.

FAQ

How do I apply online for the Bank of Ireland Platinum Credit Card?

Can I apply in a branch or by phone instead of online?

How long does it usually take from application to receiving the card?

Who is eligible to apply for the Platinum card in the Republic of Ireland?

What documents will I need for the application?

What is the Representative APR and how does it affect me?

Does the Platinum card have an annual fee and other charges?

What travel and purchase protections are included with the card?

Are there rewards, cashback or partner offers with this card?

How do I register and manage the Platinum card online and via mobile app?

What security features protect me from fraud or unauthorised transactions?

How can I improve my chances of approval before applying?

What common mistakes should I avoid on the application?

What should I do if my application is declined?

How does the Platinum card compare to other Bank of Ireland or Irish credit cards?

Are supplementary cards available for family members and what are the rules?

Will applying for the card affect my credit score?

How do I make repayments and what happens if I miss a payment?

Where can I find the most up‑to‑date interest rates, fees and insurance terms?

Content created with the help of Artificial Intelligence.