This short guide explains how to apply for the Bank of Ireland Classic Card and what to expect at each step. It is a friendly, step-by-step introduction for adults living in Ireland who are considering a basic Bank of Ireland credit card for everyday purchases, travel and credit-building.

Classic

You will find clear advice on preparing documents, choosing an application route — whether to apply online, visit a branch or phone the bank — and how to manage the card after approval. The article explains typical Bank of Ireland card procedures and common Irish regulatory requirements, but you should check Bank of Ireland’s website or contact the bank for the latest terms, APRs and fees.

Anúncios

The content that follows is organised into 11 sections covering features, eligibility, the Bank of Ireland credit card application process, fees, security and alternatives. Follow this guidance to prepare for a smooth Bank of Ireland credit card application and to decide if the Bank of Ireland Classic Card suits your needs.

Key Takeaways

- The Bank of Ireland Classic Card is aimed at adults in Ireland seeking a straightforward credit card for daily use and travel.

- Learn how to apply for Bank of Ireland Classic Card online, in-branch or by phone and gather required documents in advance.

- Check eligibility, fees and representative APRs on the Bank of Ireland site before you complete any Bank of Ireland credit card application.

- Preparing proof of identity, proof of address and income speeds up approval for an apply Bank of Ireland Classic Card Ireland application.

- Use the upcoming sections to compare features, manage the card after approval and explore alternatives if needed.

IRELAND: STEP-BY-STEP GUIDE – How to Apply for the Bank of Ireland Classic Credit Card

Looking for a straightforward credit card with no annual bank fee in Ireland? This walkthrough explains exactly how to apply for the Bank of Ireland Classic Credit Card.

Anúncios

Why Consider the Classic Credit Card?

The Bank of Ireland Classic Credit Card is a widely chosen option for day-to-day spending.

Its key advantages include:

- No annual bank fee (only the mandatory €30 Government Stamp Duty applies)

- Introductory promotions such as 0% interest on purchases or balance transfers for a limited period

Before You Apply: Basic Requirements

To qualify, you must:

- Be at least 18 years old

- Live in the Republic of Ireland

- Have a minimum yearly income of €16,000

- Provide valid proof of identity and address

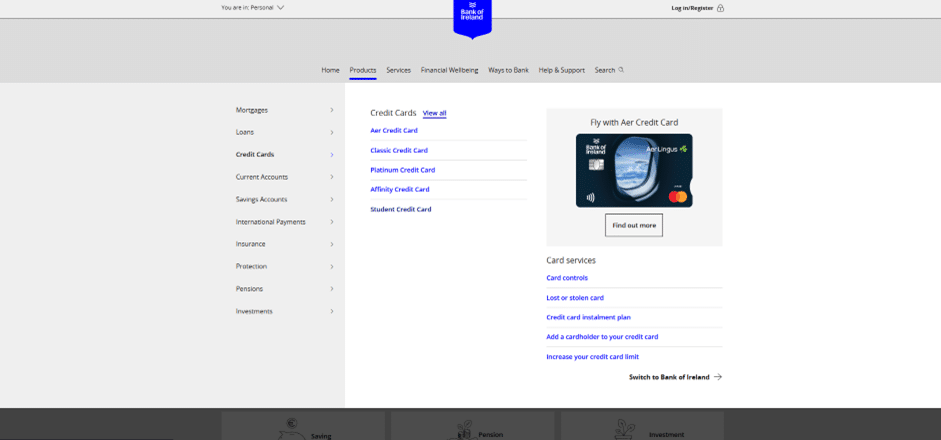

Step 1: Open the Bank of Ireland Credit Cards Section

Start your application directly on the official Bank of Ireland website.

- Go to the Bank of Ireland Personal Banking homepage.

- In the main navigation menu, click “Borrow” (or “Products”, depending on the layout).

- In the submenu, choose “Credit Cards” and then select “View all” or “Compare Credit Cards”.

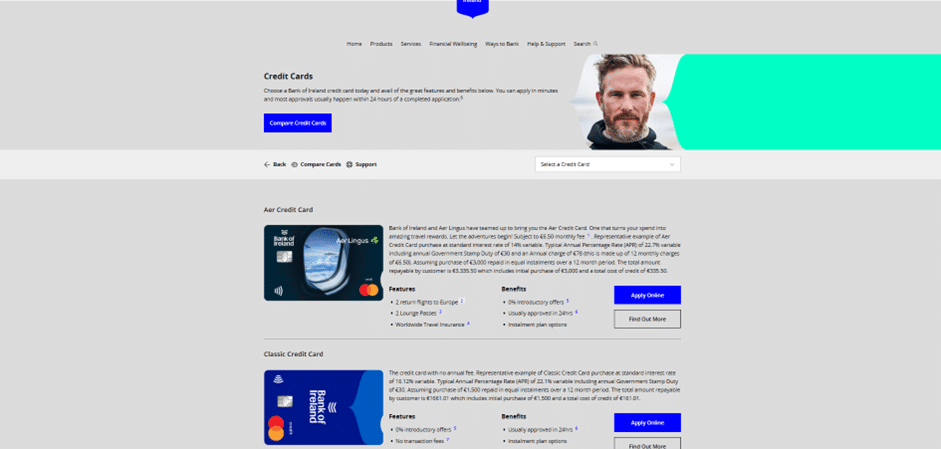

Step 2: Choose the Classic Credit Card

In the comparison area, you will see several card options (Aer, Platinum, Student, etc.).

- Look for the Classic Credit Card, generally the second option on the list.

- Click “Find out more” to open its detailed page.

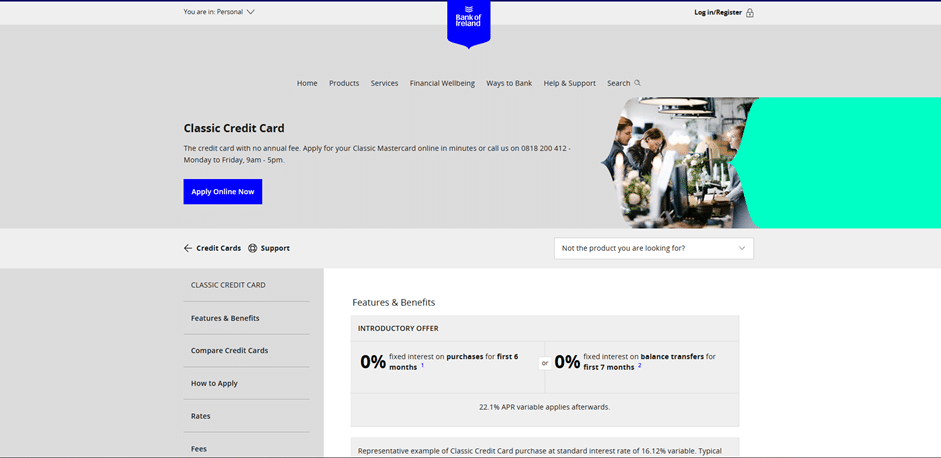

Step 3: Start the Online Application

You are now viewing the Classic Card’s information page.

Here, you’ll find details such as:

- Representative APR: 22.1% variable

- Introductory offers (commonly 0% for 6 months on purchases or 0% for 7 months on balance transfers)

To continue, click the blue “Apply Online Now” button.

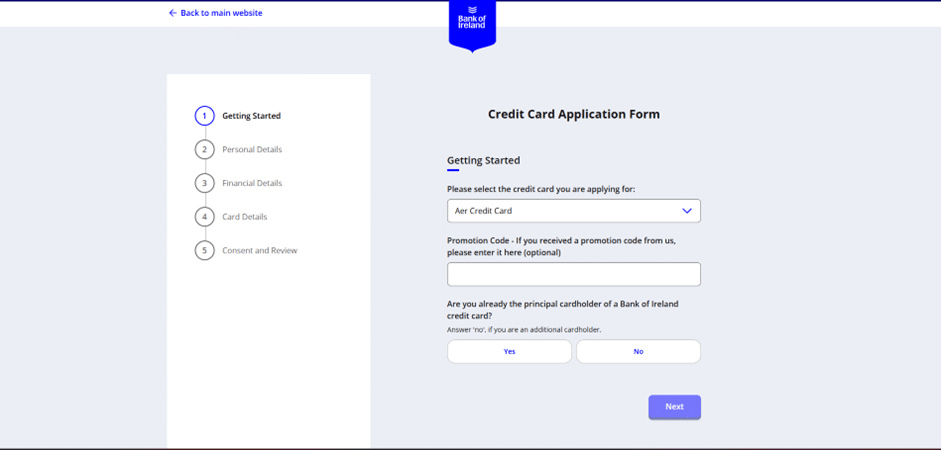

Step 4: Fill Out the Application Form

You will be redirected to the online application platform.

- If you already use 365 Online, the process is faster. In many cases, approval can be granted within 24 working hours if all documents are provided.

- Enter your personal information, income details, and housing history.

- Upload or submit any required documents as instructed.

Once everything is completed, submit your application. You will then receive a decision from Bank of Ireland regarding your Classic Credit Card.

Bank of Ireland Classic Card — learn how to apply for this card.

The Classic Card is an entry-level credit option from Bank of Ireland designed for everyday spending. It offers standard credit limits, contactless payments and basic travel and purchase protections. For many customers this card balances simple features with straightforward costs.

Typical Classic Card features include chip-and-PIN security, online and mobile banking access, monthly statements and emergency card replacement. Balance management tools help you track spending. Note that extras such as travel insurance or cashback depend on the specific product version and eligibility; check the current Bank of Ireland literature for details.

Bank of Ireland eligibility normally requires applicants to be aged 18 or over and resident in the Republic of Ireland with a verifiable address. The bank carries out a credit assessment that looks at credit history, income and existing debts. Those with limited or poor credit may receive lower limits or be declined.

Non-residents or temporary residents should contact Bank of Ireland before applying, as rules can differ. Proof of identity and address will be needed during the process, and income verification may affect the outcome.

Many people choose Classic Card when they want a simple, low-cost credit option for daily purchases or to build credit. When you compare benefits, the Classic Card has fewer perks than premium Bank of Ireland cards but often carries lower fees and simpler eligibility.

If you want travel cover, extensive rewards or business features, review the Bank of Ireland card comparison to see which product fits best. For everyday use and straightforward terms, some customers will decide to choose Classic Card as the right fit.

Key benefits of the Bank of Ireland Classic Card for everyday use

The Classic Card delivers practical features for everyday spending. It balances simplicity with helpful protections and modest perks that suit many customers in Ireland.

Purchase protection and travel conveniences

Cardholders receive basic purchase protection that can assist with unauthorised transactions and disputes. Short-term purchase protection or extended warranties may apply to some items, depending on the merchant and product terms. Always keep receipts and check specific cover limits before claiming.

The card is accepted where Mastercard or Visa is taken, giving reliable travel conveniences worldwide. Contactless payments speed up small purchases. When abroad, Bank of Ireland can arrange emergency cash or card replacement under its emergency procedures, subject to verification and local availability.

Do not assume travel insurance is included. Many basic cards lack comprehensive cover. If you need robust travel protection, confirm your policy details or arrange separate travel insurance.

Interest rates and credit limits explained

Representative APR shows the typical annual cost of credit for outstanding balances. The exact interest rates you receive depend on your creditworthiness and current product terms offered by Bank of Ireland.

Credit limits are set after assessing income, credit history and existing liabilities. New accounts often start with modest limits. Customers can request an increase later if circumstances change and credit checks support it.

Interest may apply from the transaction date for purchases not cleared by the statement due date. Cash withdrawals usually attract immediate interest plus fees. Check your statement and the card terms to see how interest charges are calculated.

Loyalty rewards and partner offers

The Classic Card is primarily a basic credit product, so loyalty rewards are limited compared with premium cards. If ongoing points or cashback are a priority, consider higher-tier options.

Bank of Ireland occasionally runs partner offers and merchant promotions for cardholders. Availability and value can vary. Review current promotions and read the terms to understand eligibility and redemption rules before relying on an offer.

Eligibility criteria and required documentation

The Bank of Ireland Classic Card has clear rules on who can apply and what documents are needed. Read these points before you start an application to avoid delays. Meeting the eligibility criteria Bank of Ireland helps speed up decisions and sets realistic expectations about credit limits.

Age, residency and credit history requirements

Applicants must normally be at least 18 years old to apply. The bank usually requires a permanent Irish residential address. People living and working in Ireland on valid visas may be considered, but they should confirm eligibility with Bank of Ireland first.

Bank of Ireland runs a credit check through Irish credit bureaus. A history of defaults, county court judgments or bankruptcy can affect approval or the credit limit offered. Honest disclosure of financial commitments improves assessment accuracy.

Proof of identity and proof of address acceptable in Ireland

You must provide proof of identity Ireland that clearly shows your name and photo. Typical documents include a valid passport, an Irish driving licence, an Irish passport card or an EU national identity card.

Proof of address Ireland must be dated within the timeframe set by the bank, usually within the last three months. Acceptable items include a recent utility bill for gas, electricity or landline, a bank statement showing your address, a mortgage statement or official government correspondence.

New residents may be asked for a tenancy agreement or employment letter alongside photographic ID. Bank of Ireland will list any additional acceptable documents at application.

Income verification and employment details

Income verification for credit card applications is required to assess affordability. Employed applicants typically supply one or two recent payslips, a P60 or recent bank statements that show salary credits.

Self-employed customers should provide accounts, SA302 tax records or a letter from an accountant. Bank of Ireland may request employer name, job title, length of employment and contact details to confirm work status.

How to apply online for the Bank of Ireland Classic Card

Applying for a Bank of Ireland Classic Card online is straightforward when you prepare ahead. This short guide walks you through what to gather, how to complete the form and simple tips to speed approval. Use the online application walkthrough below to make the process smooth.

Bank of Irland

Preparing your documents and information

Gather photographic ID such as a passport or driving licence and a recent proof of address like a utility bill or bank statement. Have your latest payslips or other income evidence ready. Keep your PPS number and details of existing debts and monthly outgoings to hand.

Ensure Bank of Ireland online banking credentials are available if required. Check that your phone number and email are current. Consider running a personal credit check so you can address any issues before you apply.

Step-by-step walkthrough of the online application form

Start by selecting the Classic Card product on the Bank of Ireland site. Enter personal details: full name, date of birth and current address. Provide employment, income data and declare other credit commitments.

Upload documents where prompted or choose to present them in branch if you prefer. Agree the terms and give consent for a credit check. Automated checks may verify identity and address instantly. A manual review can follow if the bank needs extra evidence.

Decisions can be instant, same day or take a few working days depending on verification. Once approved, card dispatch usually follows within the timescale stated by the bank.

Tips to speed up approval and avoid common mistakes

Match names and addresses exactly to what appears on your ID and proof of address. Provide complete income details and declare all credit commitments to avoid delays. Use clear, legible scans or photos for uploads.

Respond promptly to any requests from Bank of Ireland for further information. Apply when you can provide recent documents, such as the latest payslip, so the bank does not request updated evidence later.

Following this online application walkthrough and taking time to prepare documents credit card applicants will reduce friction and improve the odds when they apply online Bank of Ireland Classic Card.

How to apply in-branch and by phone

Visiting a local Bank of Ireland branch or applying by phone gives a personal option for your credit application. Booking an appointment reduces wait time and helps staff prepare for your visit.

Booking an appointment at a local branch

Find your nearest branch using Bank of Ireland’s branch locator or call the branch directly to schedule a time. Appointments often avoid queues and let staff allocate the right adviser for a credit query.

Pick quieter hours such as mid-morning on weekdays. Bring all documentation to avoid a follow-up visit and to speed up any decision on-site.

What to bring to your branch appointment

Prepare the essential documents before you arrive. Bring photographic ID, for example a passport or driving licence, plus proof of address such as a recent utility bill or bank statement.

Have proof of income ready: a recent payslip, a P60 or relevant tax documentation. Keep your PPS number accessible and recent bank statements if the adviser asks for them.

Bring records of any existing credit commitments and a mobile device for e-signature or online verification if branch staff request it. This helps the adviser process the application faster.

Applying by phone: what to expect and verification steps

The phone application credit card process begins with eligibility questions and the adviser collecting personal and financial details. You will be asked to consent to a credit search during the call.

After the call, you may need to upload documents securely, post copies or visit a branch for verification. Bank of Ireland might follow up with a call to confirm identity or clarify details.

Decisions by phone can be quick when records match and documents are provided promptly. If further checks are required, expect standard processing times for a full outcome.

| Step | What to expect | Tip |

|---|---|---|

| Find and book | Use branch locator or call to secure an appointment | Choose mid-morning slots for shorter waits |

| Documents to bring | Photographic ID, proof of address, proof of income, PPS number | Bring recent bank statements and device for e-signature |

| Phone application | Eligibility checks, credit search consent, data collection | Have documents ready to upload or post after the call |

| Verification | Follow-up by secure upload, post or branch visit; possible verification call | Respond quickly to requests to speed up approval |

| Timeline | Quick if records match; standard processing if additional checks needed | Bring everything at first visit to avoid delays |

Understanding fees, interest rates and charges

The cost of using a credit card is rarely limited to the advertised rate. Before applying, check the full tariff so you know which Bank of Ireland fees may apply to your Classic Card. A clear grasp of the annual charges, penalty costs and other levies helps you avoid surprises and manage borrowing more confidently.

Many cards carry an annual fee while basic options may have no fee or a modest charge. Penalty charges can include late payment fees, over-limit fees and returned payment charges. Each amount and trigger is shown in the card terms and conditions, so read them carefully to see what could affect your account.

Representative APR

Representative APR shows the annualised cost of credit, combining interest and certain fees into one figure. The rate you are offered will depend on your credit profile, so applicants with stronger histories may receive lower representative APRs.

Interest calculation

Interest on purchases is usually applied when a balance is carried beyond any interest-free period. Cash advances attract interest immediately. Interest calculation often uses the outstanding daily balance and the monthly billing cycle to determine charges.

Example: carry a £500 balance with a 19.9% representative APR and no interest-free period. The card will calculate daily interest on the outstanding balance, add it up for the billing cycle and post a monthly interest charge. Small changes to the daily balance change the final amount you pay.

Foreign transaction fee

Using the card abroad or on non-sterling purchases can incur a foreign transaction fee. This is typically a percentage of the transaction value and may reflect whether the card runs on the Visa or Mastercard network. Some banks add a conversion margin on top of network fees, so confirm the exact rate for your card.

Cash withdrawal charges

ATM cash advances on a credit card tend to carry higher charges. You will usually see an immediate fee plus interest from the date of withdrawal. These cash withdrawal charges far exceed standard purchase costs, so avoid using the card for cash unless absolutely necessary.

To keep costs low, consider paying balances in full each month, choose a card with low foreign transaction fees for travel and avoid cash advances. Check the Bank of Ireland fees schedule regularly to spot any changes that affect your account.

| Charge type | Typical cost | When it applies |

|---|---|---|

| Annual fee | None to modest annual amount | Yearly, depends on card tier |

| Late payment fee | Fixed penalty per missed payment | When a minimum payment is late |

| Over-limit fee | Fixed fee or declined transaction | When spending exceeds the credit limit |

| Representative APR | Variable; example 19.9% APR | Applied to carried balances and some fees |

| Interest calculation method | Daily balance × daily rate | Used to compute monthly interest |

| Foreign transaction fee | Typically 1%–3% of transaction | Non-sterling purchases or conversions |

| Cash withdrawal charges | Fixed fee plus higher interest | ATM cash advances and similar services |

Managing your Bank of Ireland Classic Card after approval

Once your Classic Card arrives, activate it straight away. Activation can be done by phone, at an ATM or through the Bank of Ireland mobile app following the bank’s instructions. Keep the temporary sleeve or any old cards secure until you destroy them.

Activating your card and setting a PIN

Follow the activation steps shown with your card. If you choose phone activation have your card number and customer details ready. ATM activation often lets you set PIN instantly.

Where permitted, use the app to set PIN choices or to change them later. Never share your PIN with anyone and avoid easy combinations. Memorise the code and destroy any notes with the number.

Online banking, mobile app and account alerts

Register for online banking if you have not done so. The Bank of Ireland mobile app gives quick access to balances, transactions and statements. Use it to make payments and to check recent activity.

Switch on account alerts to receive push or email notices for transactions, low balances and payment reminders. Alerts aid fraud detection and help with monthly budgeting. Enable biometric login and two-factor options for stronger security.

Setting up direct debits and making repayments

Decide how you will clear the balance. You can set up repayments direct debit from a Bank of Ireland current account or a nominated bank account. Choose to pay the full balance each month where possible to avoid interest.

Manual payments may be made online, by phone, at a branch or by post. Check your statement date and the payment due date so funds clear on time. Confirm processing times and make sure there are sufficient funds to avoid returned payments and penalty charges.

| Task | How to do it | Benefits |

|---|---|---|

| Activate card | Phone, ATM or Bank of Ireland mobile app | Use card straight away; prevents fraud on new card |

| Set PIN | ATM or in-app where available | Secure purchases and cash withdrawals |

| Enroll for online banking | Register online or at a branch | View transactions, download statements, manage settings |

| Enable account alerts | Turn on push or email alerts in app or online | Instant fraud alerts; payment reminders; budgeting help |

| Set up repayments direct debit | Link to a current account and confirm amounts | Automatic payments; reduces missed payments and fees |

| Make manual payments | Online, phone, branch or post | Flexible control over payment amounts and timing |

Security, fraud protection and customer support

The Bank of Ireland takes card security seriously and offers practical steps to keep your account safe. This section explains chip-and-PIN and contactless security, how to report lost or stolen cards, and what happens when you raise a dispute. Read the short guidance and keep the emergency numbers to hand.

Chip-and-PIN and contactless security measures

EMV chip technology and PIN entry form the core defence against counterfeit and skimming fraud. The chip creates a unique code for each transaction, which makes cloned cards ineffective. Use chip-and-PIN for higher-value payments or where the terminal requests verification.

Contactless offers quick payments for low-value purchases. Contactless security limits the amount per tap and often requires a PIN after a number of transactions. For online shopping, Bank of Ireland supports 3D Secure services such as Verified by Visa and Mastercard SecureCode to authenticate merchants and reduce fraud.

Regularly check your account and enable transaction alerts. Small habits, such as covering the PIN pad and reviewing monthly statements, improve your card security Bank of Ireland.

Reporting lost or stolen cards and emergency assistance

If your card is lost or stolen, contact Bank of Ireland immediately via the 24/7 lost & stolen helpline to block the card and arrange a replacement. You should report lost card incidents without delay to limit any unauthorised use and to meet bank liability rules under Irish consumer protection.

Travel customers can request emergency replacement or a temporary cash advance where available. Keep emergency contact details and follow up with written confirmation if the bank asks for additional information.

How Bank of Ireland handles suspected fraud and disputes

Report disputed transactions as soon as you spot them. Bank of Ireland investigates under established banking and payments procedures and may issue a provisional refund while it seeks evidence. Typical timelines vary, but the bank will advise on next steps and keep you informed.

You may need to supply transaction details, receipts or any police reports in cases of serious fraud. Specialist teams at Bank of Ireland manage investigations and communicate outcomes and remedies under regulatory frameworks.

| Action | Who to contact | Typical response |

|---|---|---|

| Block lost or stolen card | 24/7 lost & stolen helpline | Immediate block and replacement ordered |

| Report unauthorised transaction | Secure message via online banking or phone | Investigation started; provisional refund possible |

| Request emergency cash while abroad | Customer support team | Temporary cash assistance or emergency card issued |

| Dispute outcome follow-up | Fraud investigation team | Formal outcome and any recompense explained |

Alternatives to the Classic Card and comparison with competitors

Exploring other options helps you pick the right plastic for your spending. Bank of Ireland card alternatives range from entry-level student and low-rate cards to feature-rich Gold and Platinum products. Each option has different rewards, limits and fees, so take time to check what matches your habits.

Other Bank of Ireland card options and upgrades

Bank of Ireland offers upgrade paths for customers with a solid repayment record. A typical route moves from a Classic or student card to Gold, then to Platinum where travel insurance and concierge services are common perks.

Ask about eligibility criteria before applying for a higher tier. Reward programmes, annual fees and credit limits vary by product and can affect the value you get from an upgrade.

Comparing with credit cards from other Irish banks

It pays to compare credit cards Ireland when choosing a new card. Major competitors include AIB, Permanent TSB and KBC where available. Look at representative APRs, annual fees, foreign transaction costs and customer support ratings.

Use a side-by-side checklist for total cost of ownership and benefits. Third-party comparison tools can speed this up, but always verify terms on the issuer’s website before you commit.

When to consider a debit card, prepaid card or other credit products

Weigh debit versus credit card for everyday use. Debit cards access funds directly, so there is no interest charge and little risk of overspending. Fraud protections differ from credit cards, so check your bank’s safeguards.

Prepaid cards Ireland suit travellers or people who want strict budgets and no credit check. They may carry top-up or ATM fees, so compare costs before you buy.

Other credit products such as personal loans or authorised overdrafts may be better for planned large purchases or consolidation. Compare rates, flexibility and early repayment penalties to find the best fit for your needs.

Conclusion

The Bank of Ireland Classic Card is a straightforward credit option for everyday spending, offering standard security features and familiar benefits. This Bank of Ireland Classic summary shows the card is accessible through online, in-branch and phone applications, with clear eligibility and documentation requirements for residents of Ireland.

Before you apply, prepare photographic ID, proof of address and income documents, and choose the application route that suits you best. If you want extra perks, compare fees, representative APR and features against other cards; this helps you decide whether to apply Bank of Ireland Classic Card conclusion or look for a different product.

Practical tips: check Bank of Ireland’s latest terms and representative APR before submitting an application, monitor statements regularly and set up account alerts, and contact Bank of Ireland immediately if your card is lost or you suspect fraud. For guidance on how to apply credit card Ireland, follow the bank’s step‑by‑step instructions and keep copies of all documents.

This guide aims to make the process simple and transparent. For the most current, binding details, always consult Bank of Ireland directly or visit their official channels before you finalise any application.

FAQ

What is the Bank of Ireland Classic Card and who is it for?

What are the main features I can expect with the Classic Card?

Am I eligible to apply for the Classic Card?

What identification and proof of address do I need?

What income documents are required to prove affordability?

How do I apply online and how long does approval take?

Can I apply in branch or by phone instead of online?

What fees and interest should I expect with the Classic Card?

Are there foreign transaction fees or extra charges when travelling?

How do I activate the card and set a PIN after approval?

How can I manage my card online and set alerts?

What should I do if my card is lost or stolen while travelling?

How does Bank of Ireland handle suspected fraud and disputes?

Can I request a credit limit increase or upgrade to another Bank of Ireland card?

How does the Classic Card compare with other Irish banks’ cards?

When might a debit card, prepaid card or personal loan be a better option?

Where can I find the most up‑to‑date terms, APRs and tariffs for the Classic Card?

Content created with the help of Artificial Intelligence.