This short guide explains what you need to know about the Bank of Ireland Aer Lingus Card and how to apply for Aer Lingus card options in Ireland. It covers eligibility, the main card types, travel perks, and step‑by‑step instructions for the Aer Lingus credit card application. Whether you are weighing up an AerClub credit card Ireland to boost points on flights or comparing a Bank of Ireland travel card with other rewards cards, this article will help you decide.

Aer

The aim is practical. You will find clear advice on who can apply, what documents to prepare, and how to submit an online or in‑branch application. The guide also explains key features such as AerClub points, travel insurance and everyday spending tips to make the most of the Aer Lingus credit card application once approved.

Anúncios

The tone is friendly and targeted at adults resident in the Republic of Ireland who already understand basic credit card concepts. Read on for simple, reliable steps to apply for the Bank of Ireland Aer Lingus Card and to check whether it suits your travel and spending habits.

Key Takeaways

- The Bank of Ireland Aer Lingus Card helps you earn AerClub points on everyday spending.

- You can apply for Aer Lingus card online, by phone or at a Bank of Ireland branch.

- Prepare proof of identity, address and income for a smooth Aer Lingus credit card application.

- Compare card types and fees to choose the right Bank of Ireland travel card for your needs.

- Use smart spending and seasonal offers to maximise AerClub credit card Ireland rewards.

IRELAND: STEP-BY-STEP GUIDE – How to Apply for the Bank of Ireland Aer Credit Card

If you’re searching for a credit card that rewards you for travelling, this guide will show you how to apply for the Aer Credit Card—offered through a partnership between Bank of Ireland and Aer Lingus.

Anúncios

Why Choose the Aer Credit Card?

The Aer Credit Card enables you to earn Avios points on everyday spending.

It’s designed for frequent travellers and includes valuable perks such as:

- Two return flights to Europe after spending €5,000 in a year

- Fast Track and Priority Boarding passes

- Worldwide multi-trip travel insurance

Before You Begin: Requirements

To apply, you must:

- Be at least 18 years old

- Have been living in the Republic of Ireland for at least 6 months

- Be enrolled in AerClub (Aer Lingus’s loyalty programme)

- Provide proof of identity and address for verification

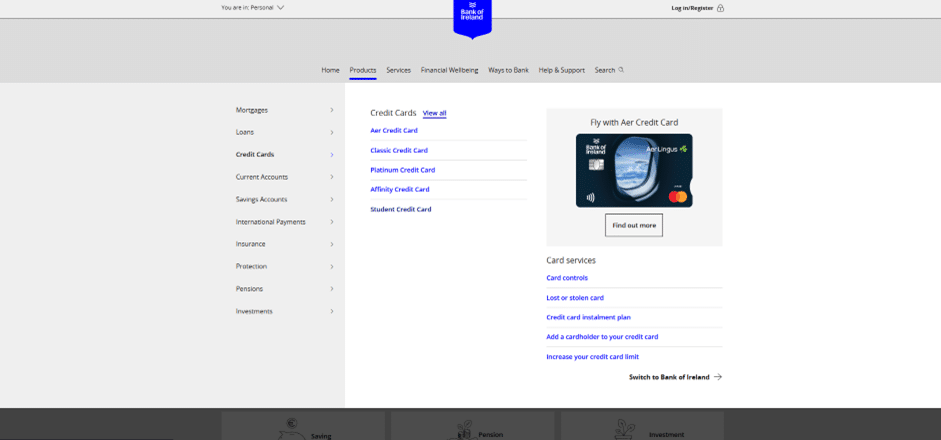

Step 1: Go to the Bank of Ireland Credit Cards Section

Start your application on the official Bank of Ireland website.

- Visit the Bank of Ireland Personal Banking homepage.

- From the main navigation menu, select “Borrow” (or “Products”, depending on the layout).

- In the submenu, click “Credit Cards”, then choose “View all” or “Compare Credit Cards”.

Step 2: Choose the Aer Credit Card

On the credit card comparison page, find the Aer Credit Card.

You’ll see various options such as the Classic, Platinum, and Student Cards.

- Select the Aer Credit Card—usually listed first

- Click “Find out more” to open the card details page

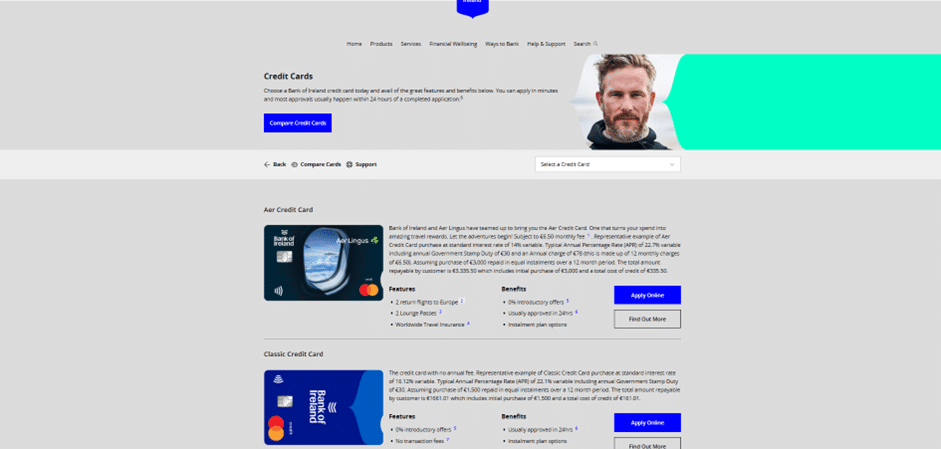

Step 3: Start the Online Application

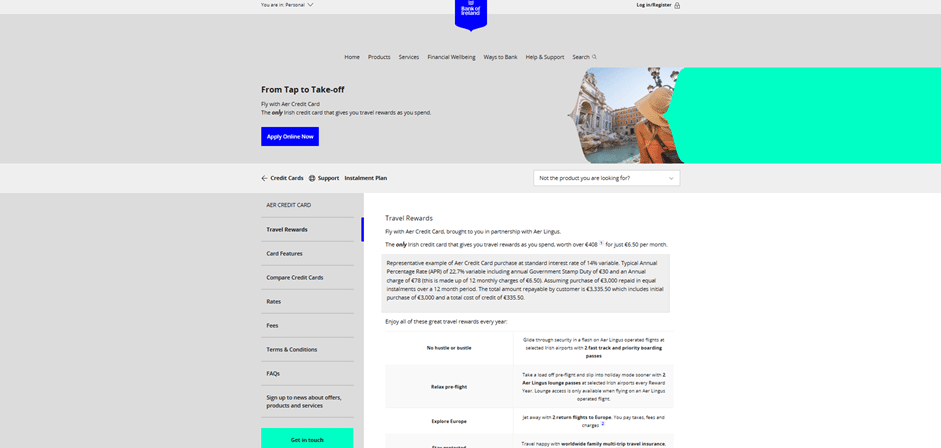

You will now be on the Aer Credit Card information page.

Here you can review details such as:

- Travel benefits

- Monthly fee (around €6.50)

- Representative APR (typically around 14% variable)

To proceed, click the blue button labelled “Apply Online Now” or “Apply for an Aer Credit Card”.

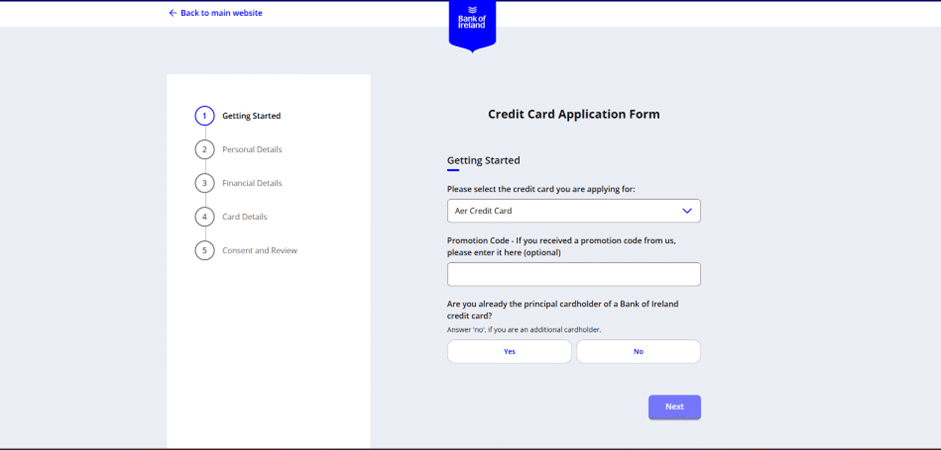

Step 4: Fill Out the Application

You will be taken to the online application platform (sometimes managed in partnership with Aer Lingus).

- Existing Bank of Ireland customers may be approved faster—often within 24 working hours if documents are complete.

- You will need to provide your personal information, financial details, and AerClub membership number.

Submit all required documentation and follow the prompts until completion.

After submitting your application, you will shortly receive an update on your application status.

Bank of Ireland Aer Lingus Card — learn how to apply for this card.

The co‑branded Bank of Ireland Aer Lingus card links everyday spending to AerClub points that can be redeemed for flights, upgrades and partner rewards. This AerClub credit card overview explains typical features such as points on regular purchases, introductory or promotional offers where available, companion flight promotions for some card variants, and travel insurance or purchase protection that often accompanies the product.

Exact earning rates, fees and perks vary with Bank of Ireland’s current product terms and the AerClub programme rules. Applicants should check Bank of Ireland and Aer Lingus for the latest terms before applying. The card suits customers who want a straightforward route to Aer Lingus loyalty benefits through routine spending.

Overview of the card

The card converts qualifying spend into AerClub points with bonus rates for travel-related purchases in some versions. Welcome offers can boost initial point balances, while ongoing promotions may add extra value during seasonal campaigns. Travel perks may include priority boarding or companion discounts depending on the variant chosen and current promotions from Aer Lingus.

Who is eligible in Ireland

Eligibility Bank of Ireland card Ireland normally requires applicants to be at least 18 and resident in the Republic of Ireland with an Irish address. Bank of Ireland will assess affordability, employment status and income to set a suitable credit limit. A satisfactory credit record is usually needed; applicants without sufficient credit history or non‑residents may not qualify.

AerClub membership is commonly required to collect points. Joining AerClub is free and takes only a few minutes online, so new cardholders can link accounts and start earning AerClub points promptly after activation.

Why apply: main travel and loyalty benefits

Primary motivations include earning AerClub points on everyday and travel spend, redeeming points for flights or cabin upgrades, and using included travel insurance and purchase protection. Regular flyers and families who use Aer Lingus can build rewards faster than with non‑co‑branded cards.

Bank of Irland

The value of the card depends on your spending habits, travel frequency and how efficiently you redeem rewards. Those who focus spending on the card and make regular Aer Lingus bookings will see the best return from Aer Lingus loyalty benefits and related travel perks.

Key benefits of the Bank of Ireland Aer Lingus Card for Irish travellers

This card helps regular travellers earn AerClub points and enjoy practical travel perks. The page below explains how points are earned, which travel perks Aer Lingus card holders may receive, and the insurance and purchase protection features that come with the account.

AerClub points earning rates and examples

Co‑branded cards normally give higher AerClub points rates for Aer Lingus tickets and a standard rate for everyday spend. Typical structures offer 2 AerClub points per €1 on Aer Lingus purchases and 1 point per €1 on general spend, though rates may vary at application.

Example: a €200 return flight earning 2 points per €1 returns 400 AerClub points. A month of groceries totalling €1,000 at 1 point per €1 yields 1,000 points. Check current Bank of Ireland terms for exact earning rates, caps and any introductory bonus offers before applying.

Travel perks and companion offers

Some card variants include travel perks Aer Lingus card holders value, such as priority boarding or lounge access on premium tiers. Perks differ by card level and may be subject to activation or minimum spend rules.

A companion offer AerClub promotions sometimes provide a discounted or free seat for a second passenger on selected routes. Taxes and carrier charges usually remain payable for the companion. Read the terms to confirm eligible routes and booking windows.

Members can also earn points with Aer Lingus partners, including IAG airlines, hotels and car hire firms. Partner earnings increase value when you combine flight spend with hotel or rental bookings.

Insurance and purchase protection features

Card benefits often include travel insurance credit card Ireland buyers want: single‑trip or annual cover, travel delay, baggage delay and rental car collision cover on some variants. Cover levels and eligibility vary by card and insurer.

Purchase protection can cover theft, accidental damage and offer extended warranty or refund protection for items bought on the card. Limits and exclusions apply, so hold the product documents when making claims.

Types of Bank of Ireland Aer Lingus Card options and compare features

Bank of Ireland usually offers a range of AerClub-linked cards to suit different needs. Expect entry-level, reward and premium options. Each variant balances points earning, travel perks and the annual fee Aer Lingus card holders might pay.

Card variants and how they differ

Standard cards often give modest AerClub points on everyday spend and charge a low or no annual fee. Reward or classic variants lift the points rate and may include companion vouchers or priority boarding. Premium cards push the highest earning rates, include airport lounge access, and offer enhanced travel insurance.

Some products are credit cards, while others may be debit-linked or charge cards. Confirm the exact product type on Bank of Ireland’s product pages before applying to ensure the features match your needs.

Fees, interest rates and credit limits explained

The annual fee Aer Lingus card attracts should be weighed against the value of points and benefits. Promotional offers sometimes waive the fee in the first year.

Representative APRs and credit card interest rates Ireland vary by card and personal profile. Interest on purchases normally accrues if you carry a balance after the statement due date. Cash advances tend to have higher rates and extra fees, and interest starts immediately.

Credit limits are set by Bank of Ireland after they assess your income, affordability and credit history. Limits can differ widely between applicants and across Aer Lingus card types.

Which card suits different traveller profiles

Frequent flyers who redeem points often should consider premium options. These are likely the best travel card for frequent flyers because they boost earnings and add perks such as lounge access and companion vouchers.

Occasional travellers and those on tighter budgets will find standard or low‑fee cards more suitable. They earn AerClub points on everyday spending without a high annual commitment.

Families may prioritise companion offers and family-friendly insurance. Business travellers might value flexible redemption, purchase protection and comprehensive travel insurance. Students and new credit customers should choose lower-fee cards to build credit while collecting points.

| Variant | Typical annual fee | Points earning | Common perks | Who it suits |

|---|---|---|---|---|

| Standard | Low or no annual fee | Basic AerClub points on spend | Purchase protection, basic travel cover | Occasional travellers, students |

| Reward / Classic | Moderate annual fee | Higher points rate on select categories | Companion vouchers, priority boarding | Regular leisure travellers |

| Premium | Higher annual fee | Top-tier points on most spend | Lounge access, enhanced insurance, concierge | Frequent flyers, business travellers |

Eligibility criteria and required documentation for applicants in Ireland

Before you start a credit application Ireland, it helps to check basic eligibility and gather paperwork. This makes the process smoother and raises your chance of approval for an AerClub card. The main checks cover age, residency, credit history and affordability under Bank of Ireland lending rules.

Age, residency and credit history requirements

Applicants must usually be aged 18 or over and resident in the Republic of Ireland with a verifiable address. Bank of Ireland will carry out a credit check via Irish credit reference agencies. Recent defaults, County Court Judgements or persistent arrears can affect AerClub card eligibility and may lead to reduced limits or refusal.

Affordability checks look at your income, outgoings and existing debts. A stable income and manageable debt levels improve your chances. Self-employed applicants should expect more detailed scrutiny of business finances.

Documents to prepare before applying

Having the required documents Bank of Ireland seeks saves time. Typical items include proof of identity such as a passport or driving licence, proof of address like a utility bill dated within the last three months, and proof of income such as recent payslips, a P60, or bank statements.

For those who are self-employed, supply recent tax returns, audited accounts or a Revenue statement. Include details of existing debts and credit commitments. If you are already an AerClub member, add your membership number. If not, registering is free and simple before you apply.

Common reasons applications are declined and how to avoid them

Common causes of refusal include insufficient income, poor credit history, too many recent credit applications and incomplete or inconsistent application information. Affordability concerns also account for many declines.

To reduce the risk of rejection, check your credit report and correct any errors before you submit a credit application Ireland. Ensure all income documents are current and accurate. Limit multiple simultaneous applications and work to lower outstanding balances on existing credit to improve affordability metrics.

| Issue | What Bank of Ireland checks | How to prepare |

|---|---|---|

| Age & residency | Minimum age and Irish residential address verification | Have passport/driving licence and a recent utility bill ready |

| Credit history | Credit reference check for defaults, CCJs and payment trends | Order a credit report, correct errors and avoid new credit before applying |

| Income & affordability | Proof of sustainable income and assessment of existing debt | Gather payslips, P60 or bank statements; reduce outstanding balances |

| Self‑employed applicants | Detailed review of tax returns and business accounts | Provide recent Revenue documents or audited accounts |

| AerClub membership | Membership number can be linked for rewards | Join AerClub in advance if you do not have a number |

| Application errors | Inconsistent or incomplete data can trigger declines | Double‑check all fields and upload clear documents |

If an application is declined, you may ask Bank of Ireland for the reasons and request a copy of the credit reference check under Irish data protection rules. Understanding the cause allows you to address issues and reapply when circumstances improve.

Step-by-step guide on how to apply online for the Bank of Ireland Aer Lingus Card

Ready to apply online Aer Lingus card? This short guide walks you through each stage so you can complete the Bank of Ireland online application with confidence. Keep documents close and follow the simple checks below to avoid delays.

Preparing your information and documents

Gather your passport or driving licence and a recent utility bill or bank statement for proof of address. Have payslips or a P60 ready to show income. Keep your bank account details and AerClub membership number to hand to speed up the process.

Check your credit report for accuracy before you start. Make sure name, address and contact details match your ID documents. Scan or photograph documents in accepted formats so you can upload them quickly during the Bank of Ireland online application.

Navigating the online application form

Begin by entering personal details, then add employment and income information. Declare any existing credit commitments. Choose the card variant that suits you and confirm your AerClub number when prompted.

Review fees, interest and the terms shown on screen. You will be asked to consent to a credit check. Note that Bank of Ireland usually carries out a full credit check rather than a soft search.

Use a secure connection and ensure you are on the official Bank of Ireland site. Never share passwords or One Time Passwords (OTPs) with anyone.

What to expect after submission and typical approval times

Some applications give an instant decision. Others move to a manual review and can take several working days. The bank may request further documents or clarification during verification.

Once approved, full approval and card dispatch often complete within 5–10 working days, though times can vary. On receipt, activate your card, set a PIN and link it to your AerClub account.

If you need help with how to apply credit card Ireland or prefer phone support, Bank of Ireland customer services can guide you through the final steps and registering for online banking to manage your AerClub card online.

How to apply by phone or in branch for customers who prefer personal support

If you prefer a guided approach, you can choose to apply by phone or visit a branch for an in‑person discussion. Calling or attending a branch lets you ask specific questions about AerClub earning rates, fees and insurance before you commit. Staff will outline the application steps and confirm what documents are needed.

Contacting Bank of Ireland customer service

Find the right phone number on the Bank of Ireland website under the customer service section. Lines usually open during standard business hours and offer options to speak to a representative about product features, eligibility and the application process. When you call, an agent can explain that a telephone application may require verbal consent to a credit check and can confirm the documents you must provide.

Use the call to clarify any current promotions or to request special assistance. If you want to apply by phone Bank of Ireland staff can take details, advise on next steps and note any follow‑up paperwork you must submit.

Visiting a branch: what to bring and questions to ask

For a Bank of Ireland branch application bring photographic ID such as a passport or driving licence, a recent utility bill for proof of address and proof of income like payslips or bank statements. Having recent Bank of Ireland statements helps if staff need to verify your account history.

Ask clear questions: confirm the annual fee and interest rates, check exact AerClub earning rates, review insurance coverage, learn how companion offers work and request expected approval times. If you prefer a focused meeting, arrange an appointment for a dedicated advisor session.

Assistance for existing Bank of Ireland customers

Existing customers often enjoy faster identity verification and may see pre‑qualified offers in online banking. You can apply through online banking, by phone banking or request a tailored discussion at your local branch. Linking a new card to your current accounts makes setting up direct debits and receiving statements simpler.

Branch staff can use your customer records to expedite verification during an in‑branch credit card application. If you need help, ask your branch for details about any customer benefits or expedited processes available to existing account holders.

Maximising AerClub points and making the most of the card

Use your Bank of Ireland Aer Lingus card with intent to build balance quickly. Focus routine spend where the card gives the best return. Small habit changes add up and help you maximise AerClub points over months rather than years.

Everyday spending strategies

Concentrate groceries, fuel and recurring bills on the Aer Lingus card where it pays to do so. Set direct debits for subscriptions and pay them with the AerClub card when secure. Shift large one‑off purchases to the card, then clear the balance each month to avoid interest. Watch bonus categories and move spend to the card during promotional windows to earn AerClub points Ireland faster.

Promotions and partner earning opportunities

Sign up to Aer Lingus and Bank of Ireland newsletters to catch limited offers. They run targeted promotions and accelerated earning periods that boost returns. Look for partner earning AerClub deals with hotels, car hire firms and retail partners within IAG. Timing stays and rentals around promotions can multiply point accrual.

Practical partner tips

- Check partner rates before booking so you know when to use the card or pay another way.

- Follow Aer Lingus and Bank of Ireland on social channels for flash deals and exclusive codes.

- Use hotel and car hire partners listed by AerClub to capture companion earning AerClub bonuses.

Best ways to redeem points

Reward flights often give the best value per point. Be flexible with dates and nearby airports to improve availability. Combining cash+points can reduce outlay on off‑peak trips and help you redeem AerClub points for travel sooner.

Upgrades and family pooling

Plan ahead for Aer Lingus upgrades points redemptions; cabin upgrades sell out quickly on popular routes. Use family accounts or point pooling when allowed to gather enough balance for long‑haul or peak‑season travel. Check AerClub rules regularly for transfer and pooling conditions.

Small adjustments to spending, alertness to promotions and smart redemption planning will help you maximise AerClub points and get the most from the Aer Lingus card.

Fees, interest and managing repayments responsibly

Understanding the costs linked to your Bank of Ireland Aer Lingus Card helps you use it with confidence. Read each point to know how annual charges, interest and extra fees can affect your balance. Use the bank’s tools to manage payments and protect your credit rating.

What you pay each year depends on the card tier. Premium variants often carry higher annual fees but add perks such as lounge access and bonus AerClub points. Promotional offers sometimes waive the first-year fee. Check the current schedule with Bank of Ireland to compare value.

The representative Bank of Ireland APR applies to purchases when you do not clear the balance by the due date. Cash advances attract higher rates and fees, and interest usually starts immediately. Other potential charges include foreign transaction fees, cash advance fees, returned payment fees and replacement card fees. Always verify the published fee table before you travel.

Tips to avoid interest and late payment fees

Try to pay the full balance each month to avoid interest. If that is not possible, pay more than the minimum to cut interest costs faster. Set a direct debit for the minimum amount to stop missed payments. Make sure you keep enough funds in the linked account to prevent returned payment charges.

Avoid cash advances unless there is no alternative. They carry higher charges and interest accrues at once. Track statement dates and set calendar reminders so due dates are not missed. Small, regular payments between statements reduce the balance and lower interest when you cannot pay in full.

Using online banking and alerts to manage your account

Register for Bank of Ireland online banking and the mobile app to view transactions and make payments on the go. Use the app to download statements and check your points balance alongside spending. These tools help you manage repayments Ireland without hassle.

Enable credit card alerts by push, SMS or email for payment due dates, large purchases and unusual activity. Alerts help you spot fraud early and keep you on top of bills. Set budgeting limits and use any transaction categorisation features to monitor spending and boost AerClub points without overspending.

| Area | What to watch for | Practical action |

|---|---|---|

| Annual fee | Higher on premium cards; first-year waivers may apply | Compare benefits to fee; check current offers from Bank of Ireland |

| Interest (Bank of Ireland APR) | Applied if balance not paid in full; higher on cash advances | Pay full balance monthly or increase payments above minimum |

| Other fees | Foreign transaction, cash advance, replacement card, returned payments | Review fee schedule before travel; avoid cash withdrawals on card |

| Missed payments | Late fees, interest, credit score impact | Set up direct debit for at least the minimum; keep sufficient funds |

| Account management | Monitor transactions, payments and points | Use online banking, app and credit card alerts for real-time updates |

Security features and card protection for peace of mind

Bank of Ireland builds several protective layers into its Aer Lingus card to help keep your money and data safe. Fraud monitoring runs 24/7 to spot unusual spending and flag suspicious activity. Cardholders may receive an alert or a call from the bank to verify a transaction and limit exposure to unauthorised charges.

Fraud monitoring and liability protection

The bank uses chip and PIN technology alongside contactless limits to reduce in-person fraud. Online account management benefits from two-factor authentication when available. If unauthorised transactions occur and you have not contributed to the fraud, liability is typically limited under Bank of Ireland fraud protection rules.

Travel disruption and purchase insurance included

Many card variants include travel disruption insurance that covers trip cancellation, curtailment, travel delay and baggage loss or delay. Cover levels and exact terms depend on the specific card and insurer, so check the policy wording before you travel.

Purchase protection Ireland provisions often cover accidental damage and theft for items bought with the card. Extended warranty cover may be available on qualifying purchases. Keep receipts and records when you buy items so claims can be supported quickly.

What to do if your card is lost or stolen

If your card goes missing, call the dedicated lost and stolen line shown on Bank of Ireland’s site immediately to block the card. Follow the bank’s instructions to request a replacement and ask about emergency cash or a temporary card if you are abroad.

Review recent transactions and report any unauthorised charges straight away. Update or pause recurring payments and linked services once your replacement arrives to avoid missed subscriptions. Familiarise yourself with lost card procedures before travel for faster action when you need it.

Comparing the Bank of Ireland Aer Lingus Card with other travel cards in Ireland

Choosing between airline co‑branded cards and flexible reward cards comes down to your routes, spending and how you redeem points. This short guide will help you compare travel cards Ireland, weighing AerClub benefits against rival programmes and general rewards options.

AerClub card versus other airline‑branded cards

Bank of Ireland’s Aer Lingus card links directly to AerClub points. Cards that earn Avios or other frequent flyer currencies work differently when it comes to earning structure, partner networks and redemption charts. For example, Avios is strong for British Airways and Iberia routes, while AerClub fits Aer Lingus routes and partners in the oneworld and partner network.

When looking at AerClub vs Avios consider seat availability, taxes and route coverage. Companion offers, lounge access and included travel insurance vary by issuer and card level. Higher‑tier airline co‑branded cards often give better travel perks but cost more in annual fees.

Non‑airline travel cards and general rewards cards comparison

Flexible points programmes such as bank reward currencies or Amex Membership Rewards let you shift value between airlines, hotels and travel partners. That flexibility can beat airline points for travellers who do not stick to one carrier.

Cashback cards and simple points cards prize ease of use. They convert spending into cash or statement credits. For many users, straightforward cashback offers clearer value than airline points that require searching award availability.

Which card is best depending on travel frequency and spending habits

If you fly Aer Lingus often and redeem regularly, an AerClub card can yield high value and targeted perks. Frequent flyers who favour multiple carriers should lean towards flexible rewards or cashback cards for broader redemption options.

Do the maths: estimate annual spend, apply earning rates, subtract annual fees and estimate redeemable value per point. This rewards card comparison will show which product gives the best net benefit for your travel pattern.

| Card type | Best for | Earning focus | Typical perks | Ease of redemption |

|---|---|---|---|---|

| Bank of Ireland AerClub card | Regular Aer Lingus travellers | AerClub points on Aer Lingus and partners | Companion offers, flight rewards, some insurance | Good for Aer Lingus routes; limited outside network |

| Avios‑earning airline cards | Those flying British Airways, Iberia or partners | Avios on flights and selected spend | Lounge passes at higher tiers, tier points | Strong on oneworld routes; award availability varies |

| Flexible points cards (bank/Amex) | Multi‑carrier travellers and hotel bookers | Transferable points to multiple airlines/hotels | Transfer partners, hotel bookings, greater flexibility | High if partners match your needs; needs planning |

| Cashback and general rewards cards | Simpler value seekers and casual travellers | Cashback or straightforward points | No fuss redemptions, lower complexity | Very easy; value is clear and liquid |

Conclusion

The Bank of Ireland Aer Lingus Card delivers clear value for travellers who want to collect AerClub points and enjoy travel perks. This AerClub card Ireland summary shows the essentials: you earn points on everyday spending, benefit from travel protections and companion offers, and can choose a card variant that fits your budget and travel habits.

Eligibility in Ireland is straightforward for residents with a suitable credit history. If you decide to apply for Bank of Ireland Aer Lingus Card, you can complete the online form or visit a branch with proof of ID and address. Existing customers may find in‑branch or phone support helpful during the process.

When weighing is Aer Lingus card right for me, consider travel frequency, typical monthly spending and how often you redeem points for flights or upgrades. Factor in any annual fee and make use of the insurance and purchase protections to get full value. For next steps, check the Bank of Ireland product page for current terms and rates, gather your documents, contact Bank of Ireland with pre‑application questions and join AerClub so you can start earning as soon as your card is active.

FAQ

What is the Bank of Ireland Aer Lingus Card and who issues it?

Who is eligible to apply for this card in the Republic of Ireland?

What documents should I prepare before applying online or in branch?

How do AerClub points earning rates work and can you give an example?

Are there annual fees and interest charges to consider?

What travel perks and insurance come with the card?

How do I apply online and what happens after I submit my application?

Can I apply by phone or at a branch instead?

What are common reasons applications get declined and how can I avoid this?

How can I maximise AerClub points with this card?

What are the best ways to redeem AerClub points earned on the card?

How should I manage repayments to avoid interest and fees?

What security protections are included and what should I do if my card is lost or stolen?

How does the Bank of Ireland Aer Lingus Card compare with other travel or airline cards in Ireland?

Where can I find the most up‑to‑date terms, earning rates and contact details for applying?

Content created with the help of Artificial Intelligence.