This short guide introduces the AIB Platinum Visa Card, a premium personal credit card from Allied Irish Banks aimed at customers in Ireland seeking travel benefits, purchase protection and enhanced security. It summarises what to expect from the full guide and provides the meta title and meta description to help orientate readers.

Meta title: Learn all about it and see how to apply for the AIB Platinum Visa Card — AIB Platinum Visa Card guide for Ireland.

Anúncios

AIB Platinum Visa Card

The AIB Platinum Visa Card sits in the market as a higher-tier AIB credit card that targets salaried professionals, frequent travellers and anyone who wants stronger purchase protections. This article aims to explain features and benefits, outline eligibility and fees, guide you through the AIB credit card application process, offer tips to improve approval chances and compare the card with alternatives in the Irish market.

Target audience: residents of Ireland aged 18 and over, employed or with regular income, who value travel insurance, purchase cover and robust security features. Use this guide to decide whether to apply AIB Platinum Ireland and to follow the step-by-step application advice later in the article.

Anúncios

Key Takeaways

- The AIB Platinum Visa Card is a premium AIB credit card with travel and purchase benefits.

- This guide explains eligibility, fees and how to apply AIB Platinum Ireland.

- Ideal for residents in Ireland aged 18+, salaried professionals and frequent travellers.

- Includes practical steps for a successful AIB credit card application.

- Compares the card with alternatives to help you choose the right product.

How to Apply for the AIB Platinum Visa Card

- Go to the AIB Website

Visit the official AIB website and navigate to the Credit Cards section.

- Select the AIB Platinum Visa Card

Click on the AIB Platinum Visa Card option to learn about its features, benefits, and eligibility criteria.

- Check Your Eligibility

Make sure you meet the requirements, such as age, income, and residency, before starting your application.

- Prepare the Required Documents

Gather your identification (passport or ID card), proof of income (like payslips or bank statements), and proof of address.

- Complete the Online Application

Fill in the online application form with your personal and financial details. Ensure all the information is accurate. - Submit Your Application

Review your details carefully and submit the application for processing. You’ll receive a confirmation once it’s submitted.

- Wait for the Bank’s Response

AIB will review your information. You’ll be contacted by email or phone once your application has been approved. - Receive and Activate Your Card

After approval, your AIB Platinum Visa Card will be mailed to you. Follow the activation instructions provided to start using your card and enjoy its exclusive benefits, including cashback rewards.

Learn all about it and see how to apply for the AIB Platinum Visa Card

This AIB Platinum overview explains what the card offers and who it suits in Ireland. The Platinum Visa from Allied Irish Banks is a premium credit card that bundles travel insurance, purchase protection and contactless payments. Typical Platinum perks include higher insurance limits, stronger purchase cover and, where available, travel assistance or concierge support.

Credit limits vary by applicant. AIB sets limits based on income, credit history and its lending policy. Specific benefits, terms and insurances are governed by AIB’s card terms and any third‑party insurers, so check the latest product literature before applying.

Read on for targeted guidance. The following headings break the topic into clear parts so you can decide if the card matches your needs and how to apply with confidence.

Overview of the AIB Platinum Visa Card

The AIB Platinum Visa Card is aimed at customers who want a higher‑tier credit card with travel and purchase protections built in. Travel insurance typically covers trip cancellations, delayed flights and emergency medical costs abroad. Purchase protection can include cover for theft, damage or extended warranty on eligible buys. Contactless technology makes everyday payments faster while card security features protect against fraud.

Who this card is best suited to in Ireland

Frequent travellers who value bundled travel insurance and overseas medical cover will find this card attractive. Shoppers who want purchase protection and extended warranty benefits are likely to benefit too. The card suits customers willing to pay a potential annual fee in return for those bundled services, and those who meet AIB’s minimum income and credit criteria.

What to expect from this article

This AIB card guide Ireland lays out the full picture. You will find sections on benefits, eligibility, fees, how to apply and practical tips to improve your approval chances. Later parts cover account management, comparisons with other cards and real customer experiences.

Practical next steps are simple: check if you meet the eligibility points, gather required documents and follow the step‑by‑step application guidance provided later in the article. Use this AIB Platinum overview and who should get AIB Platinum guidance to decide whether to proceed.

| Topic | What you’ll learn | Why it matters |

|---|---|---|

| Benefits | Travel insurance limits, purchase protection, contactless features | Helps assess value versus any annual fee |

| Eligibility | Residency, minimum income, credit checks and documentation | Prepares you for a smoother application |

| Fees & charges | Annual fee, representative APR, foreign transaction and cash advance costs | Clarifies true cost of using the card |

| How to apply | Online steps, in‑branch options and expected timelines | Makes the process straightforward and faster |

| Approval tips | Credit improvements, common decline reasons and documentation tips | Increases chances of a successful application |

| Account management | Online banking, repayment strategies and security settings | Helps avoid interest and keep your account secure |

| Comparisons | How the card stacks up against other AIB and rival bank cards | Helps pick the right card for different profiles |

| Customer experiences | Real feedback on travel, purchases and service | Gives practical insight into real‑world use |

Key benefits of the AIB Platinum Visa Card

The AIB Platinum Visa Card bundles premium protections and smart payment features for frequent travellers and everyday shoppers. Read the insurance details carefully so you know how cover works and what steps to take if you need to claim. The card’s digital controls make it easy to manage security and limits from the AIB mobile app.

AIB

Travel insurance and overseas cover details

Typically, travel insurance AIB Platinum includes overseas medical and repatriation cover, trip cancellation and curtailment, delayed luggage and flight delay benefits, plus personal liability. Cover usually applies when you pay for travel with the card or meet specified spend thresholds set by AIB.

Limits, excesses and exclusions vary by insurer and by the policy wording. Read the insurance certificate and policy terms AIB supplies so you understand caps on medical costs, any age limits and excluded activities.

To activate cover you normally need to fund travel costs using the card or pre-authorise tickets as required. Claims are handled by the appointed claims handler; keep receipts, booking confirmations and medical reports to support a claim.

Purchase protection and extended warranties

Purchase protection AIB typically covers theft or accidental damage to eligible items bought on the card for a fixed period after purchase. The exact duration varies, but a common term is 90 days from the purchase date.

Extended warranty benefits commonly add a set period to the manufacturer’s guarantee, often up to 12 months when you pay with the card. This can save on repair bills for major appliances and electronics.

Some exclusions apply. High-value items, commercial purchases and second‑hand goods are often outside cover. For claims you will usually need the receipt, proof that the item was paid with the card and, for theft, a police report if requested.

Contactless payments and security features

Contactless AIB Visa supports quick in‑store payments via tap, plus chip-and-PIN for higher-value transactions. Online purchases benefit from Visa Secure (3D Secure) authentication to reduce fraud risk.

Mobile wallet compatibility with Apple Pay and Google Pay adds convenience for contactless purchases. Account monitoring and a zero-liability approach protect you from unauthorised transactions when reported promptly.

Use AIB’s online or mobile banking to freeze a card, set alerts and view statements. These controls help you manage spend, detect unusual activity and make the most of the card’s security tools.

| Feature | Typical cover or benefit | What you must do |

|---|---|---|

| Overseas medical & repatriation | High-cost medical cover while abroad, repatriation if needed | Pay travel with card or meet spend threshold; keep medical reports |

| Trip cancellation & curtailment | Reimbursement for pre-paid trip costs for covered reasons | Retain booking confirmations and cancellation notices |

| Delayed luggage / flight delay | Fixed benefit payments for delays beyond policy threshold | Obtain carrier delay reports and retain receipts for essentials |

| Purchase protection AIB | Theft or accidental damage cover for a short period after purchase | Keep original receipt and proof of card payment; file report if stolen |

| Extended warranty | Extension of manufacturer’s warranty, commonly up to 12 months | Register product where required and retain warranty / proof of purchase |

| Contactless AIB Visa | Tap-to-pay, chip-and-PIN and online Visa Secure authentication | Register card with mobile wallet and enable alerts in AIB app |

| Fraud protection & controls | Real-time monitoring, zero-liability policies, ability to freeze card | Report unauthorised transactions promptly and use app controls |

Eligibility criteria and minimum requirements

Before you apply, check the basic rules that shape AIB Platinum eligibility. These cover age, residency, income and your credit record. Meeting these points does not guarantee approval; AIB will assess each application on its own merits.

Age, residency and employment status

The typical minimum age for an AIB credit card is at least 18, though some product terms may require applicants to be 21. Confirm the exact age requirement with AIB product terms before applying.

Applicants must be resident in the Republic of Ireland and able to provide a verified Irish address. Non‑Irish nationals living in Ireland may be eligible if they supply required immigration and residency documents.

Salaried employees, self‑employed customers and pensioners can apply. AIB examines stable income sources and recent employment history when assessing who can apply AIB card.

Minimum income and credit history considerations

AIB sets minimum income thresholds that vary by product and internal policy. Affordability checks look at income, regular monthly outgoings and existing credit commitments.

A good credit history improves the chance of approval. Punctual repayments, low credit utilisation and few recent credit enquiries work in your favour.

Recent defaults, county court judgements, repossessions or bankruptcy will affect eligibility. Each case is reviewed individually under AIB credit criteria Ireland.

Documentation you’ll need to apply

Have the following documents ready to speed up your application:

- Proof of identity: valid passport, Irish driving licence or other approved government ID.

- Proof of address: recent utility bill, bank statement or government correspondence dated within the past three to six months.

- Proof of income: recent payslips (usually the last three months), a P60 or P45 where relevant, or audited accounts/self‑assessment tax returns for the self‑employed.

- Supplementary paperwork: recent bank statements, confirmation of employment and details of mortgage or rental payments to demonstrate affordability.

Preparing these items in advance will help clarify AIB Platinum eligibility and show clearly who can apply AIB card when you submit your application.

Fees, interest rates and charges explained

Understanding costs helps you choose wisely. Below we break down the main charges linked to the AIB Platinum Visa Card so you can spot potential expenses before you apply.

Annual fee and any introductory offers

The AIB Platinum Visa Card may carry an annual fee. Check AIB’s product page for the current amount and any short-term waivers. Some customers receive a fee-free period for the first year or promotional reductions for existing AIB accountholders.

Benefits such as travel insurance or purchase protection can be tied to paying the annual fee or meeting minimum spend requirements. Confirm those conditions before relying on cover for trips or big purchases.

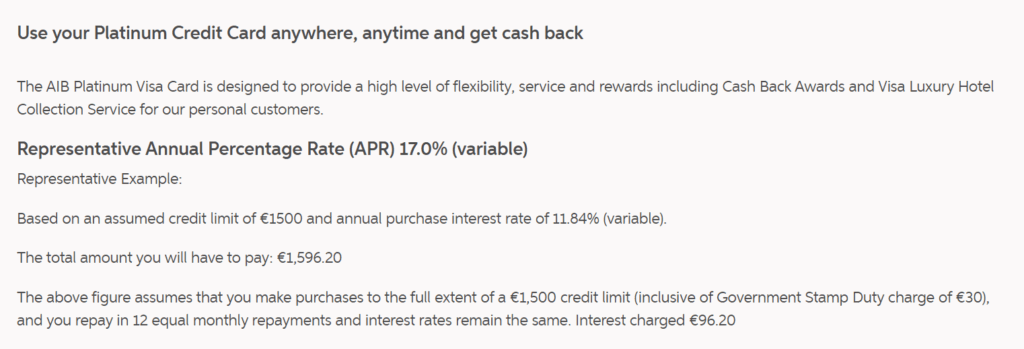

Representative APR and how interest is calculated

The advertised AIB representative APR shows the typical cost of borrowing when balances remain unpaid. The exact AIB representative APR for your application will depend on terms at the time of approval.

Interest on purchases usually starts to accrue if you do not clear the full monthly balance by the payment due date. Many cards offer a grace period on purchases when you pay in full each month. Read the card terms to confirm whether a grace period applies.

Interest is commonly calculated on a daily balance basis. The daily periodic rate comes from the APR, accrues each day, and appears as a monthly interest charge on your statement. Check AIB’s terms for precise billing cycles and calculation methods.

Foreign transaction fees and cash advance charges

An AIB foreign transaction fee typically applies when you spend in another currency or use a foreign merchant. This charge is usually a percentage of the transaction value. Verify the prevailing AIB foreign transaction fee before travel or overseas purchases.

Cash advances, such as ATM withdrawals on the credit card, attract immediate fees and higher interest rates. Interest on cash withdrawals generally begins from the withdrawal date with no interest-free period. Be aware of daily and monthly limits that may apply to cash advance transactions.

Additional charges can include late payment fees, returned payment fees and overlimit fees. Review AIB’s full fee schedule so you know where cash advance charges Ireland and other costs could affect your balance.

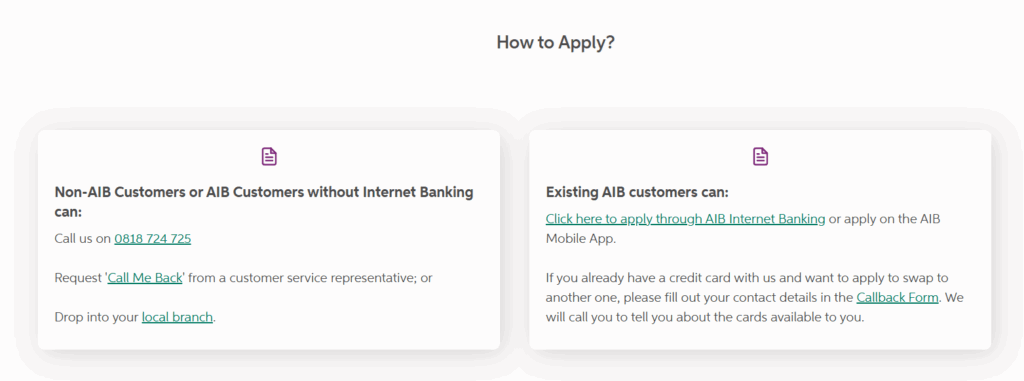

How to apply for the AIB Platinum Visa Card

Choosing how to apply for the AIB Platinum Visa Card is straightforward. You can complete the process online, visit a local branch or start by phone. Each route has simple steps and common requirements, so pick the method that suits your schedule and comfort level.

Online application process step-by-step

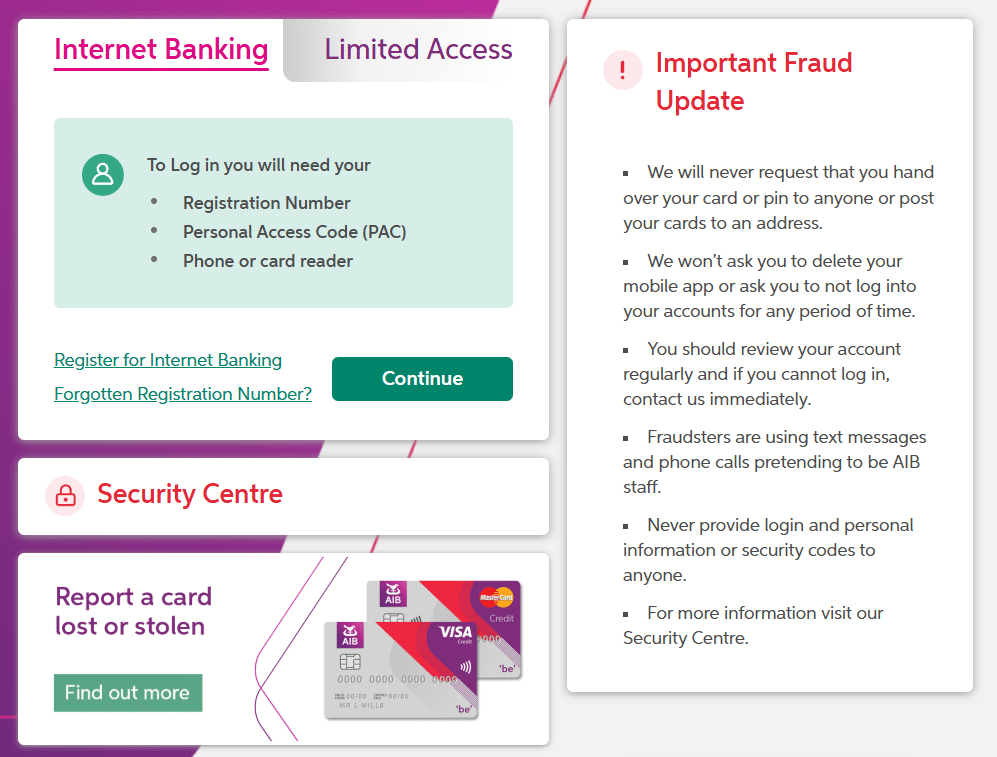

To apply AIB Platinum online, begin at AIB’s official website and find the Platinum Visa Card page. You may need to sign in or create an AIB internet banking profile before starting the secure form.

Complete the application with personal details, employment and income information, and consent to a credit check. Where the portal allows, upload identity, proof of address and proof of income documents. If upload is not available, you can post or bring them into branch later.

Check every field carefully and read the card’s terms and conditions before you submit. Accurate information cuts down on delays and supports a smoother assessment.

Applying in branch or by phone

If you prefer face-to-face help, book an appointment at an AIB branch and bring original ID, address evidence and income documents. A customer adviser can walk you through the form and submit it on your behalf.

For telephone applications, ring AIB’s personal banking line and be ready to provide identity details and consent to a credit search. Some phone-started applications may need a later branch visit for verification or document upload.

Typical application timelines and approval expectations

Online eligibility checks may give an immediate indication of success. Full approval typically takes several working days to a few weeks while AIB verifies documents and completes the credit assessment.

Delays often arise when income or address proofs are missing or inconsistent. If AIB requires extra information, they will contact you directly to request it.

On approval, the card is dispatched by post with activation instructions and policy documents for any linked benefits. Keep an eye on AIB card approval time so you can plan for card arrival and activation.

Tips to improve your approval chances

Applying for the AIB Platinum Visa Card becomes easier with a clear plan. A short check of your finances and documents helps you present a strong case. Use the steps below to improve your standing before you apply.

Improving your credit profile before applying

Order a copy of your record from the Central Credit Register or a recognised consumer credit report provider. Look for errors and correct them well before submission. Small fixes can make a noticeable difference.

Pay down existing debt and cut card utilisation to under 30% where possible. Make all payments on time and keep accounts active for several months to show stability. Avoid multiple hard credit enquiries in a short period, as these can lower your score.

Stable employment and a steady bank account history strengthen affordability checks. If you need to improve your profile quickly, target the highest-impact items first: missed payments and high balances.

Common reasons for declined applications and how to avoid them

Insufficient income and a poor payment history are common causes of refusal. High debt-to-income ratios, recent insolvency events and mismatched application details also trigger declines. Be honest and accurate when filling in all fields on the application form.

Supply complete documentation up front and choose a card that matches your current financial position. If you want to avoid declined application outcomes, consider a product with lower eligibility thresholds until your profile improves.

If a lender refuses your request, you can ask for the reasons and a copy of the credit assessment. Use that feedback to address specific issues before reapplying.

How to present your income and documentation clearly

Prepare recent payslips, P60s or self‑assessment returns in clear digital format. Label files descriptively before uploading to make verification simple for the reviewer. For self‑employed applicants, include three years’ accounts or accountant-prepared statements where available.

Attach recent bank statements to show income flow and add a short note for irregular income such as bonuses, dividends or temporary contracts. Ensure employer contact details are correct so the bank can verify employment quickly. Clear presentation reduces back-and-forth and helps the assessor trust the information provided.

| Action | Why it helps | Practical tip |

|---|---|---|

| Check credit report | Find and correct inaccuracies that lower score | Request report from Central Credit Register, correct errors promptly |

| Reduce card utilisation | Improves debt-to-income perception | Pay balances down to under 30% of limits |

| Provide clear income docs | Speeds verification and proves affordability | Upload labelled payslips, P60s or accountant statements |

| Limit hard enquiries | Avoids temporary score drops | Space applications and research via soft checks first |

| Include explanatory notes | Clarifies unusual earnings for the assessor | Attach brief note for bonuses, dividends or contract work |

Managing your AIB Platinum Visa Card responsibly

Getting control of your card starts with a few simple steps. Register for AIB Internet Banking and download the AIB Mobile Banking app. Use these to view transactions, check statements and see your available balance in real time. Activate your new card, set a secure PIN and add it to Apple Pay or Google Pay for fast contactless payments.

Setting up online banking and card controls

Open the app and follow prompts to register. You can activate cards, change PINs and link accounts without visiting a branch. Use AIB online banking card controls to temporarily block or unblock a card if you misplace it. Where available, set merchant or geographic restrictions and manage authorised users from the same menus.

Repayment strategies to avoid interest and fees

Paying the full statement balance each month avoids interest on purchases and keeps your account within the interest‑free period. If that is not possible, set a direct debit for at least the minimum payment to avoid late fees. Increasing payments above the minimum helps reduce the balance faster.

Plan for seasonal spending by building a realistic monthly budget. If you expect to carry a balance, speak with AIB about balance transfer or targeted repayment plans. Good credit card repayment strategies Ireland use include prioritising high‑rate balances and tracking due dates to stop charges from mounting.

Using alerts, contactless limits and security settings

Enable real‑time SMS or push alerts to spot unauthorised transactions quickly. Check the app for contactless limits and cumulative thresholds; these protect you from large unauthorised spend. Turn on transaction notifications so every charge triggers an alert.

Report lost or stolen cards immediately via AIB emergency numbers and review monthly statements for unfamiliar activity. Keep app and device software up to date and use strong device locks to add a further layer of security.

| Action | Where to do it | Benefit |

|---|---|---|

| Activate card and set PIN | AIB Mobile Banking app or Internet Banking | Start using the card securely; prevents unauthorised use |

| Enable transaction alerts | App settings: Notifications | Immediate fraud detection and spending control |

| Temporarily block/unblock card | AIB online banking card controls | Makes it quick to secure the account if card is lost |

| Set up direct debit | Internet Banking or branch | Prevents missed payments and late fees |

| Add to mobile wallet | Apple Pay / Google Pay via app | Fast contactless payments with added tokenisation security |

| Plan repayment schedule | Personal budget or speak to AIB | Reduces interest costs and improves credit health |

Comparing the AIB Platinum Visa Card with other cards in Ireland

Choosing a credit card means weighing perks, fees and real-world value. This section helps you compare AIB cards with rival premium offerings and match cards to typical user needs. Read on to see how the AIB Platinum fits next to other AIB options and competing premium cards from Bank of Ireland, Permanent TSB and leading fintechs.

How it stacks up against other AIB cards

The AIB Platinum offers stronger travel insurance and higher purchase protection than entry-level AIB Classic products. Annual fees rise with cover levels, so AIB Platinum vs other AIB options often means more benefits at a higher cost. Eligibility thresholds for the Platinum card can be stricter, with higher income and credit score expectations than lower‑tier AIB cards.

Comparisons with rival banks’ premium cards

Rival premium cards from Bank of Ireland and Permanent TSB vary on APRs, fees and benefits. Some cards focus on lounge access or rewards while others prioritise comprehensive insurance. When you compare Irish credit cards, check travel insurance limits and typical APRs. Fintech issuers may offer cashback or flexible rewards rather than the insurance-heavy package found on the AIB Platinum.

Which card might suit different user profiles

Frequent travellers and buyers who want embedded insurance and purchase protection often find the AIB Platinum attractive. People who prioritise cashback or travel points could prefer rewards-led cards with lower fees. Applicants with limited credit history should consider starter cards or credit‑building options before applying for a premium card to improve approval chances.

For a clear side‑by‑side view, use comparison tools and product tables from banks and independent sites to compare AIB cards, fees and benefits. That will help you judge whether the AIB Platinum vs other AIB or rival products meets your needs as the best premium credit card Ireland for your lifestyle.

Real customer experiences and case studies

The AIB Platinum Visa card prompts a wide range of feedback from Irish cardholders. Here we present concise, real-world examples that illustrate how the card performs for travel, purchases and everyday use. These snapshots draw on AIB Platinum reviews, AIB customer experiences and AIB Platinum case studies Ireland to give practical insight without jargon.

Positive travel and purchase experiences

Several cardholders report successful travel insurance claims that covered urgent medical bills while abroad. These AIB Platinum reviews often praise straightforward claim forms and timely settlement for documented expenses.

Customers who used purchase protection for damaged electronics describe clear guidance from advisors and replacement or reimbursement within expected timeframes. Cardholders mention how contactless payments and the AIB mobile app simplified tracking spending during trips and shopping sprees.

Independent platforms such as Trustpilot and banking forums contain many of these AIB customer experiences. Readers should compare those accounts with AIB’s published testimonials to form a balanced view.

Common complaints and typical resolutions

Some users raise issues about claim eligibility and delays in processing, especially where policy thresholds or exclusions were not fully understood. These points appear repeatedly in AIB Platinum reviews from customers who felt caught by fine print.

When disputes arise, most cardholders report success after contacting AIB customer services, then escalating to the bank’s complaints handling team if needed. A minority of cases reached the Financial Services and Pensions Ombudsman in Ireland, where clear documentation sped resolution.

Keeping receipts, email threads and claim reference numbers proves crucial. These records help clarify timelines and eligibility, cutting the time spent chasing decisions.

Lessons from borrowers who switched cards

Many who moved from the AIB Platinum card cite lower fees or superior rewards from rival providers as key motivators. Others wanted a card with a lower representative APR or a different travel benefits package. Reports in AIB Platinum case studies Ireland highlight these trends.

Practical advice from switchers includes doing a full cost comparison that adds annual fees and likely interest charges. Confirm eligibility for the new card and time the change so there is no gap in travel insurance cover if you rely on card-linked benefits.

Notifying AIB about a planned switch and cancelling or downgrading the old card helps avoid missed payments and confusion with recurring subscriptions.

Conclusion

Final thoughts AIB Platinum: the AIB Platinum Visa Card is a clear fit for cardholders in Ireland who travel regularly and value purchase protection and enhanced security. The card’s travel insurance, extended warranties and contactless safeguards make it a strong premium option, but these perks come with an annual fee and eligibility conditions that are worth weighing carefully.

Should I apply AIB Platinum: before you apply, check your residency and income meet AIB’s criteria and review your credit profile. Gather the documentation listed in Section 4, compare representative APRs and foreign transaction fees from Section 5, and weigh benefits against costs to decide if the card suits your spending habits.

To apply AIB Platinum Ireland, follow the step‑by‑step guidance in Section 6 or visit an AIB branch to discuss terms and view the insurance policy documents. Manage the card responsibly by paying balances in full when possible, setting up alerts and using AIB’s digital tools to control contactless limits and monitor transactions.

If the card aligns with your needs, head to AIB’s official channels to confirm up‑to‑date terms and begin the application. Taking these practical steps will help you get the most from the card while avoiding unnecessary charges and protecting your finances.

FAQ

What is the AIB Platinum Visa Card?

Who is the AIB Platinum Visa Card best suited to?

What travel insurance and overseas cover does the card provide?

How does purchase protection and extended warranty work?

What security and contactless features does the card include?

What are the eligibility criteria for the AIB Platinum Visa Card?

What documentation will I need to apply?

Are there annual fees, interest rates and other charges?

How do I apply for the card online, in branch or by phone?

How long does a typical application take?

How can I improve my chances of approval?

Why might an application be declined and what can I do?

How should I manage the card responsibly to avoid interest and fees?

What card controls and alerts are available?

How does the AIB Platinum compare with other AIB and rival premium cards?

What do real customers say about the card?

Can I add the AIB Platinum Visa Card to Apple Pay or Google Pay?

What happens to insurance cover if I switch or close my card?

Where can I find the most up‑to‑date terms and policy documents?

Content created with the help of Artificial Intelligence.