This short guide explains how to apply for AIB be Visa Card in Ireland. It draws on Allied Irish Banks’ product pages and customer support materials to give a clear, practical walkthrough of the AIB be card application process.

You’ll find straightforward steps on how to apply AIB Visa Ireland, what documents to prepare, and the choices for online or in‑branch applications. The aim is to help you move from checking eligibility to activating and using the card with confidence.

Anúncios

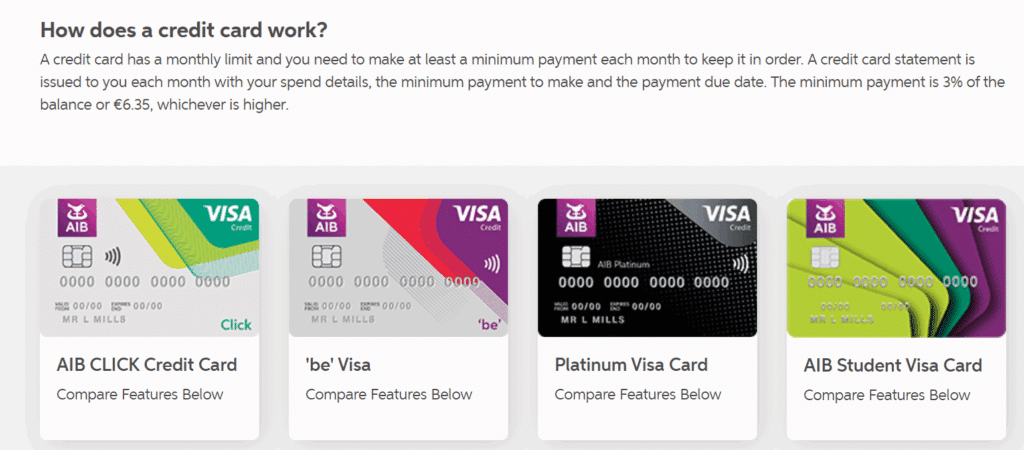

AIB 'be' Visa

Key Takeaways

- Learn the essentials for a successful AIB be card application.

- Prepare identity, residency and income documents in advance.

- Choose online or branch routes depending on convenience.

- Understand the credit assessment and common reasons for decline.

- Activate and secure your card safely once approved.

How to Apply for the AIB ‘be’ Visa Card

- Visit the AIB Website

Go to the official AIB website and open the Credit Cards section.

- Select the AIB ‘be’ Visa Card

Find and click on the AIB ‘be’ Visa Card option to view its features, benefits, and requirements.

- Check Your Eligibility

Review the eligibility criteria such as age, income, and residency to make sure you qualify before applying.

- Prepare Your Documents

Gather your personal information, proof of identity (such as a passport or ID card), proof of address, and proof of income.

- Complete the Application Form

Fill out the online form carefully with your personal and financial details. Make sure all the information is accurate.

- Submit Your Application

Double-check your data and submit the form for processing. You will receive confirmation once your application has been received. - Wait for Approval

The bank will review your details. If approved, you’ll receive a notification via email or phone. - Receive and Activate Your Card

Once your AIB ‘be’ Visa Card arrives, follow the activation instructions provided to start using it securely for your purchases.

Want to learn how to apply for the AIB ‘be’ Visa Card?

This short guide gathers practical steps and checks to help you while applying for AIB be card Ireland. It pulls together AIB’s published ID and proof rules and common Irish banking practice so you reach the application stage without delays. The process reflects Central Bank of Ireland expectations on creditworthiness and responsible lending for residents.

Why this guide is useful for applicants in Ireland

If you live in Ireland this guide saves time by listing the exact documents AIB typically asks for: valid photo ID, proof of address, and income verification. It explains common eligibility pitfalls that slow approvals and shows how to avoid them. You will get clear timelines for checks and card delivery, so you know what to expect at each step.

Anúncios

Who this card is best suited to

The AIB ‘be’ Visa Card fits people who want a straightforward credit card with contactless and mobile payments and tight integration with AIB online banking. It is ideal for salaried employees, pensioners with regular income, and many self-employed applicants who can provide accounts or tax returns. If you want premium travel rewards or concierge services, this card might not be the best choice.

Overview of the application journey

The application journey AIB card follows a clear sequence: check eligibility, gather documents, apply online or in-branch, verify identity, wait for a credit decision, receive the card, then activate and set it up. Pre-checks are often immediate, credit decisions commonly take a few days and card delivery generally arrives within five to ten working days, though timing can vary.

Overview of the AIB ‘be’ Visa Card and its benefits

The AIB ‘be’ Visa Card blends global acceptance with everyday convenience. It works wherever Visa is accepted, gives chip-and-PIN security and offers emergency card replacement and cash access when you travel. The card links to AIB mobile banking and online accounts so you can check transactions and set alerts in real time.

AIB

Key features of the AIB ‘be’ Visa Card

The card supports contactless payments for small purchases, reducing checkout time. Cardholders can set up direct debits for repayments and receive integrated monthly statements to track spending. Emergency replacement and cash access provide peace of mind on trips abroad.

Rewards, interest rates and fees

Rewards and promotional offers may change, so applicants should read the current terms. Expect representative APRs on purchases, interest on unpaid balances and higher rates for cash advances. Late payment charges and potential foreign transaction fees can apply.

Before accepting an offer, compare the AIB card fees and rates against your needs. Confirm the annual fee, any cash advance fees and penalty charges on AIB’s official rates and fees schedule.

Contactless, online and mobile features

Tap-to-pay functionality uses the contactless AIB card limit set by AIB and Visa, making small purchases faster. You can add the card to Apple Pay or Google Pay if your device supports them. Visa Secure (3-D Secure) helps protect online purchases.

Real-time alerts and spending summaries arrive through AIB mobile banking, helping you spot unusual activity quickly. Linking the card to online banking gives instant access to statements, transaction history and simple controls for card use.

Eligibility criteria for AIB ‘be’ Visa Card applicants

Before you apply, it helps to know what AIB looks for. This section explains the main checks on age, residency, income and credit history so you can prepare and avoid delays.

Age and residency requirements in Ireland

AIB usually requires applicants to be at least 18 years old and to live in the Republic of Ireland. Proof of an Irish address such as a utility bill or bank statement is normally needed. EU citizens with an Irish address and valid documentation may meet the same credit card age residency rules as Irish nationals.

Income, employment and credit history considerations

Lenders assess whether you have a regular income large enough to cover monthly repayments. Employed applicants typically supply recent payslips and employer details. Pensioners provide pension statements. Self-employed applicants submit tax returns or certified accounts to show earnings.

Credit checks are routine. Recent loan applications, missed payments, defaults, or insolvency can reduce the chance of approval. It helps to review your credit report from Irish credit reference agencies before you apply.

Common reasons applications are declined

Applications can be turned down for several clear reasons. The most common are insufficient income to meet affordability checks and a poor credit history with marked defaults or judgments. Inconsistent or incomplete documentation often causes delays or refusals.

Not meeting residency requirements is another frequent issue. Temporary visitors without proof of long-term residence usually do not satisfy AIB card eligibility Ireland rules.

| Area checked | What AIB expects | How to prepare |

|---|---|---|

| Age and residency | Applicant aged 18+ and resident in the Republic of Ireland | Provide valid ID and a recent Irish address proof |

| Income and employment | Regular income sufficient for repayments | Gather payslips, pension statements or tax returns |

| Credit history | Reasonable credit record with no recent defaults | Check and correct your credit file before applying |

| Documentation | Complete and consistent documents | Ensure names, addresses and figures match across papers |

| Affordability checks | Meet income requirements AIB and living expense assessments | Prepare a realistic budget and declare any additional income |

Documents and information to prepare before applying

Gathering the right paperwork speeds up any AIB card application. Below is a clear checklist to help you prepare proof of identity, evidence of address and income papers. Keep originals and recent copies ready to avoid delays when you apply for an AIB card.

Proof of identity and residency

Acceptable ID for credit card Ireland usually includes a valid passport or an Irish driving licence with photograph. Use the most current document you hold to avoid verification issues.

Proof of address can be a recent utility bill, bank statement or official letter dated within three months. AIB may accept local authority letters or Revenue correspondence as evidence. Present both ID for credit card Ireland and a recent address document when asked.

Income verification and payslips

Most applicants should bring recent payslips, typically the last three months, plus employer contact details. A P60 or employment contract can help when AIB requests further confirmation.

Pensioners should supply a pension award letter or bank statements showing pension credits. Bank statements that show regular income can support payslip evidence and strengthen your application.

Additional documents for self-employed applicants

Self-employed documents AIB requests include recent full accounts, tax returns such as Form 11 or a Notice of Assessment, and business bank statements. Provide details of your business structure, whether sole trader, partnership or limited company.

Up-to-date accounts or certified financials help prove ongoing trading and consistent income. Preparing self-employed documents AIB expects reduces the chance of follow-up requests and speeds up the decision.

Step-by-step online application process

Starting an application for the AIB ‘be’ Visa Card is quick when you follow a clear route. Begin on AIB’s official website or use the mobile app to locate the AIB ‘be’ Visa Card page. Look for the apply now or get started button. A simple eligibility check or soft search may be offered. This helps estimate your chances without affecting your credit score.

When you apply online AIB be Visa, take your time with each screen. Use the H3 sections below to guide you through the main steps. Accurate answers speed up processing and reduce the chance of follow-up requests.

Starting the application on the AIB website

Open the AIB site or app and sign in if you have an AIB current account. If you do not, you can proceed as a new applicant. Choose the AIB ‘be’ Visa Card and tap the apply now call-to-action.

Complete any pre-application checks. These may include an eligibility indicator or a soft credit search. Keep your passport or driving licence close by to confirm identity details.

Filling in personal and financial details accurately

Enter your full name, date of birth and address exactly as on your ID. Provide your PPS number if requested and include your current employment status. State your gross income and monthly outgoings.

List other credit commitments such as loans and existing cards. Give consent for AIB to access credit bureau information when asked. Matching names and addresses prevents delays and helps AIB make a timely decision.

Uploading documents and verifying identity online

Use AIB’s secure upload facility to submit ID, proof of address and recent payslips. Acceptable formats typically include JPEG and PDF. Check file size limits before you upload to avoid errors.

Some applicants may verify identity by linking an AIB current account or using a third-party verification service. When you upload documents AIB will review them as part of the credit decision. Keep scanned files clear and legible to speed approval.

| Step | What to have ready | Typical time |

|---|---|---|

| Pre-check | Access to AIB website or app, basic personal details | 2–5 minutes |

| Personal & financial form | Full name, PPS number, employment, income, outgoings | 10–20 minutes |

| Document upload | Passport or driving licence, utility bill, payslips or bank statements | 5–10 minutes |

| Identity verification | Link to AIB account or third-party ID check | Instant to 24 hours |

| Decision | Completed application and verified documents | Minutes to a few days |

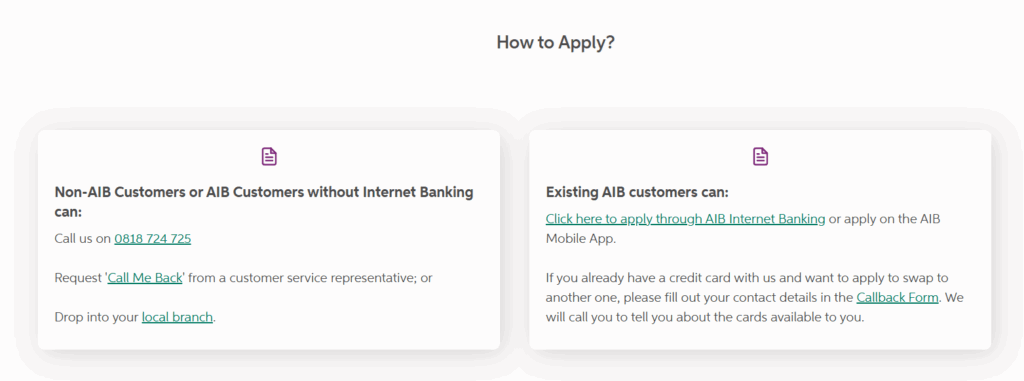

Applying in-branch or by phone: what to expect

If you prefer a face-to-face chat or a guided call, AIB offers straightforward options to apply in branch AIB or via an AIB phone application. Booking ahead makes the visit smoother and helps advisers prepare your file.

Booking an appointment with a local AIB branch

Use AIB’s branch locator to find your nearest office. You can reserve a slot online or call the branch to arrange an AIB branch appointment. Appointments reduce waiting times and ensure a staff member is available to review documents with you.

Questions the advisor will ask and documents to bring

Advisers will confirm identity, residency and employment. Expect questions about monthly commitments, salary, and why you want the card.

Bring original documents: passport or driving licence, a recent utility bill or bank statement as proof of address, recent payslips, or tax returns for self-employed applicants. Staff will photocopy or scan originals for your application.

Timeline for a decision when applying in-branch or by phone

Often you’ll receive a provisional decision during the appointment or call. If further checks are needed, a final answer may arrive within a few working days. Requests for extra documents or credit checks can extend the outcome to a week or more.

Once approved, card dispatch usually takes place within several working days. If you used an AIB phone application, expect the same verification steps and similar timelines as in-branch submissions.

Understanding the credit decision and what influences it

When you apply for a new card, the outcome rests on several clear factors. AIB looks at income, existing debts, regular living costs, employment stability and your credit history to judge affordability and set a suitable limit. Central Bank of Ireland rules mean lenders must carry out robust checks to meet responsible lending standards.

How AIB assesses creditworthiness and affordability

AIB combines the information you supply with data from credit reference agencies. They calculate whether your monthly income covers current commitments and any new repayments. A stable job history, low levels of existing debt and a tidy credit record make a positive impression.

Checking and improving your credit score before applying

Obtain your credit report from Irish credit reference agencies to check for errors or unexpected entries. Correcting mistakes can help speed approval.

Pay bills on time, reduce credit card balances and keep credit utilisation low. Registering to vote where eligible and managing overdrafts carefully give modest boosts to your profile. Avoid making several credit applications in a short period because that can hurt your score and affect improving credit score Ireland efforts.

What to do if your application is declined

If you receive a declined credit card AIB notice, ask for a formal explanation of the reasons. The bank will usually outline the key factors that influenced the decision. Request an adverse action notice so you can check your file with a credit reference agency.

You can appeal with extra documentation, apply for a lower credit limit, wait and improve your profile before reapplying, or explore other card products from different banks. Small, steady steps to clear outstanding balances and show consistent payments often change future outcomes.

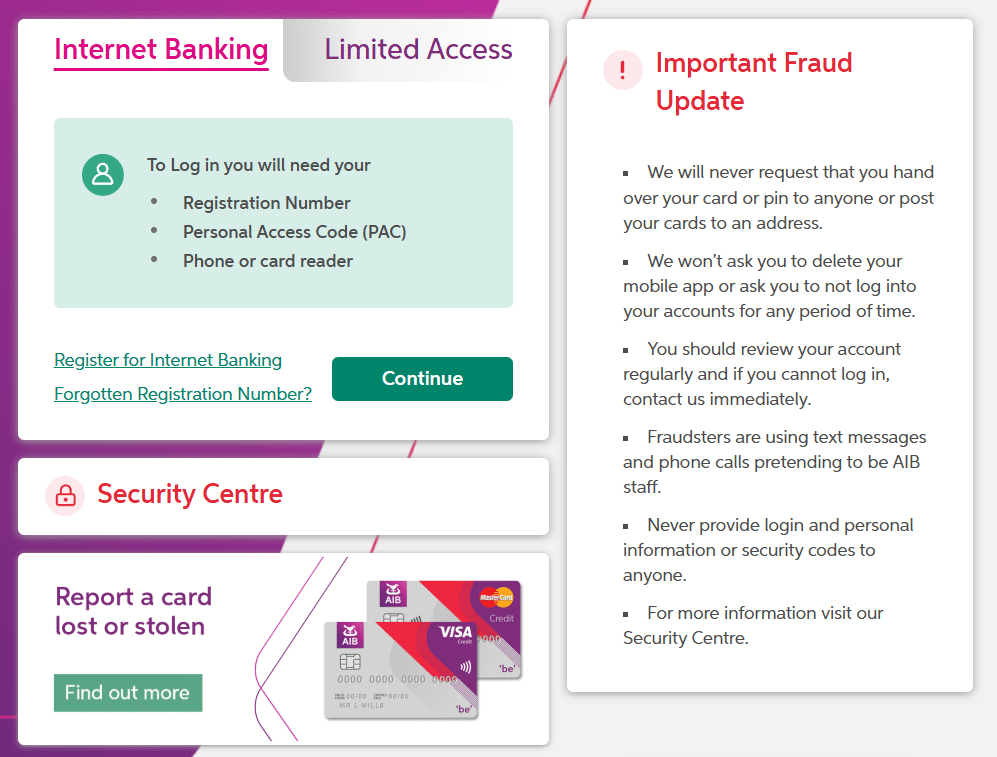

Activating and setting up your new AIB ‘be’ Visa Card

When your AIB ‘be’ Visa card arrives, take a moment to check the envelope for any tampering before you proceed. Activation and initial setup protect your account and let you start spending or adding the card to digital wallets with confidence.

The most common ways to activate AIB cards include calling the dedicated activation number, using AIB online banking, the AIB Mobile Banking app, or an AIB ATM. Follow the printed instructions that come with your card and do not activate if packaging appears opened.

How to activate your card safely

Call the number on the activation slip from a secure phone or use AIB online banking to complete activation. The AIB Mobile Banking app provides a quick route for customers who prefer mobile-first control.

Only activate once you confirm the envelope is intact. Keep any activation codes private and do not share them by text or email.

Setting up PIN, contactless limits and online banking

To set PIN AIB card, visit an AIB ATM or an AIB branch where staff can guide you securely. Choose a PIN that you can remember without writing it down and avoid obvious sequences or birthdates.

Contactless limits follow Visa and AIB policy. Use the AIB Mobile Banking setup to view your contactless settings and add spending alerts. You can adjust notifications so you have immediate awareness of contactless transactions.

Registering for mobile and online security features

Complete AIB mobile banking setup by registering in the app and enabling in-app alerts and SMS notifications. Add your card to Apple Pay or Google Pay for safer contactless payments where supported.

Turn on two-factor authentication for online banking, keep your device software up to date and use a strong password. Familiarise yourself with Visa Secure for safer online purchases and review alert preferences so you see suspicious activity straight away.

| Action | How to do it | Why it matters |

|---|---|---|

| Activate card | Call activation number, use AIB online banking, AIB app, or ATM | Starts card use and links card to your account securely |

| Set PIN | Set PIN AIB card at an ATM or in-branch | Protects chip-and-PIN purchases and ATM withdrawals |

| Manage contactless | Adjust limits and alerts in AIB Mobile Banking setup | Controls tap-to-pay spending and reduces fraud risk |

| Mobile wallet | Add card to Apple Pay or Google Pay | Makes payments faster and reduces card exposure |

| Security settings | Enable two-factor auth, update device software, set alerts | Improves account protection and detects suspicious activity |

Managing your card responsibly and making payments

Keeping control of your AIB ‘be’ Visa Card is simple when you know the repayment options and how billing cycles work. Read your monthly statement to see the minimum payment and the full balance. Mark your payment due date on a calendar so you avoid late fees and protect your credit record.

Repayment options and billing cycles

AIB offers several ways to make payments: set up a direct debit, use an online transfer, pay in-branch, or clear the balance from a linked AIB current account. Each statement shows the billing cycle and due date. Paying at least the minimum keeps your account in good standing, but clearing the full balance removes interest on purchases that have a grace period.

Tips to avoid interest and manage balances

To avoid interest AIB credit card holders should aim to pay the full statement balance every month. Cash advances attract immediate interest and extra fees, so avoid them unless there is no alternative. If you struggle to pay in full, set up an automated direct debit for the minimum and then top up when you can.

Small, regular payments help keep balances low. Review your statement for any recurring subscriptions and cancel those you no longer use. Doing this will make it easier to meet repayments and reduce the chance of incurring interest or charges.

Using AIB banking apps to track spending and set alerts

The AIB Mobile Banking app lets you monitor transactions, check balances and use temporary card controls. Turn on push or SMS notifications for payments and limits so you receive timely AIB spending alerts.

Use the app’s categorisation and budgeting tools to spot where you can cut back. Set payment reminders or an automated plan to ensure AIB card repayments arrive on time. These habits protect your credit rating and keep your account healthy.

| Topic | Action | Benefit |

|---|---|---|

| Monthly statement | Check full balance and minimum payment | Know what to pay and when to avoid fees |

| Payment methods | Direct debit, online transfer, branch, linked account | Flexible ways to make timely AIB card repayments |

| Interest avoidance | Pay full statement balance each month | Avoid interest AIB credit card charges on purchases |

| Cash advances | Use only in emergencies | Prevent immediate interest and extra fees |

| App features | Transaction categories, push/SMS alerts, temporary controls | Real-time monitoring with AIB spending alerts |

| Automation | Set direct debit or payment reminders | Reduce missed payments and protect credit |

Security, fraud protection and customer support

AIB uses several layers of defence to keep cardholders safe. Chip-and-PIN and contactless limits reduce in-person fraud. Visa Secure (3-D Secure) helps protect online purchases.

Real-time transaction monitoring flags unusual activity and can trigger SMS or app alerts. Where eligible, chargeback protection helps you contest unauthorised transactions. These measures form the core of AIB card security for everyday spending.

If your card is lost or stolen, act quickly to limit exposure. You can report lost card AIB by calling the 24/7 emergency line shown on your card literature. Blocking the card through online or mobile banking is another fast option.

When you report lost card AIB, be ready to confirm your identity and recent transactions. AIB will block the card and arrange a replacement to reduce inconvenience and liability.

For help beyond emergency action, contact AIB through several channels. Visit a local branch for face-to-face support or use AIB customer service phone lines for personal accounts. Secure messaging in internet banking and in-app chat offer private help without a branch visit.

Outside branch hours, use the dedicated emergency numbers for urgent card issues. For general enquiries, AIB customer support Ireland can assist with fraud queries, card services and account concerns.

Conclusion

This apply AIB be Visa conclusion pulls together the main steps you need: check eligibility, gather identity and income documents, choose whether to apply online or in-branch, submit accurate information and await the credit decision. Once approved, activate and set up your card securely, configure PIN and contactless settings, and use the AIB mobile and online tools to monitor activity.

For the final steps AIB card application, verify current fees and APR on AIB’s official rates and fees schedule and be honest with affordability assessments. Keep payslips and proof of address ready, monitor your credit report, and review any decline reasons before reapplying. Using AIB’s online eligibility checker can give an early indication before a full application.

Use this AIB be Visa summary as a practical checklist when preparing to apply in Ireland. Contact AIB directly for product-specific questions or current offers, and make use of digital security features to protect against fraud. With careful preparation and responsible repayment habits, the application process should be straightforward and manageable.

FAQ

What is the AIB ‘be’ Visa Card?

Who is the AIB ‘be’ Visa Card best suited to?

What are the basic eligibility requirements?

What documents do I need before applying?

Can I apply online and how long does it take?

What happens during the credit assessment?

Why might an application be declined?

What should I do if my application is declined?

How can I verify my identity when applying online?

What is the in-branch application process like?

How do I activate my new AIB ‘be’ Visa Card?

How do I set or change my PIN and contactless settings?

How can I add the card to Apple Pay or Google Pay?

What fees and interest should I expect?

How can I avoid paying interest on purchases?

What tools does AIB provide to help manage spending?

How do I report a lost or stolen card?

What fraud protection and security features are in place?

If I’m self‑employed, what extra paperwork might AIB ask for?

Can I request a different credit limit after approval?

Where can I get more help or customer support?

Conteúdo criado com auxílio de Inteligência Artificial